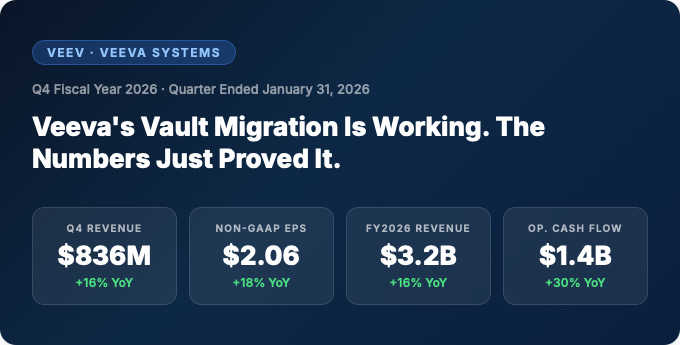

Veeva's Vault Migration Is Working. The Numbers Just Proved It.

Q4 FY2026 beat across the board. Vault CRM momentum is accelerating. The $6B path to 2030 is on track.

Veeva Systems reported fiscal Q4 2026 earnings after the bell on Wednesday, and the results weren't just a beat — they were a statement. Revenue grew 16%, non-GAAP EPS beat by $0.12, and management guided full-year FY2027 above consensus. But the story underneath the numbers is about something more durable: Vault CRM is working, and the migration off Salesforce is accelerating.

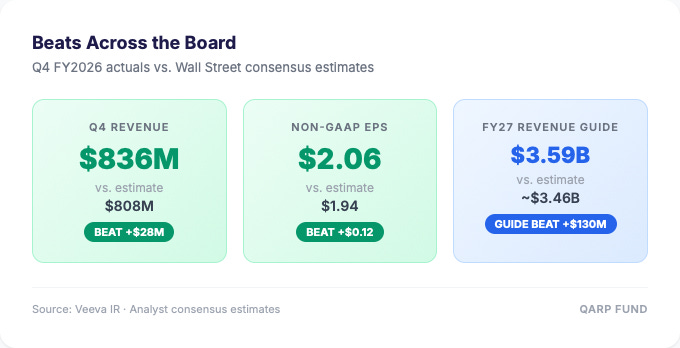

Clean Beats on Every Line

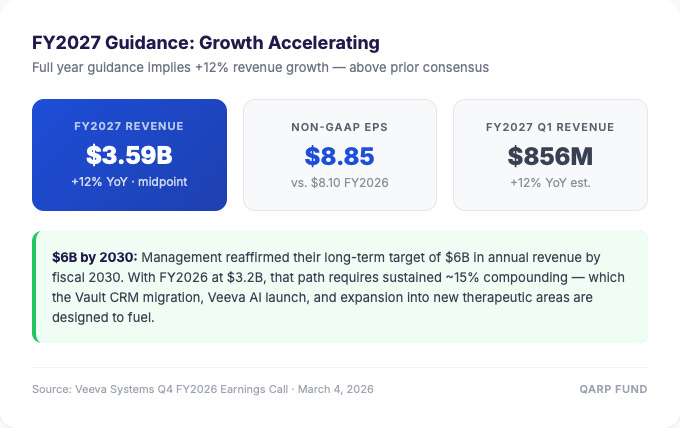

Q4 revenue came in at $836 million, up 16% year-over-year and $28 million ahead of Wall Street's estimate. Non-GAAP EPS of $2.06 beat the $1.94 consensus by $0.12 — a meaningful margin for a company that typically guides conservatively. The bigger beat came in guidance: FY2027 revenue is guided to $3.585–$3.600 billion, roughly $130 million above what the Street was expecting.

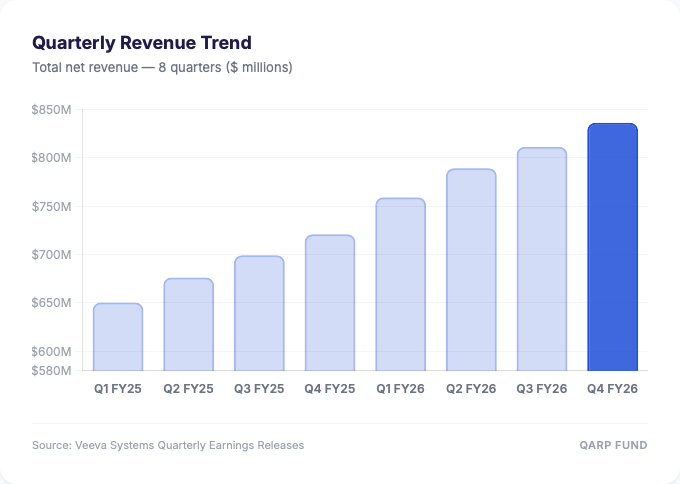

Revenue Growth Has Reaccelerated

Veeva grew at 16% in Q4 FY2026 — consistent with the pace of the last four quarters. What matters here isn't just the absolute growth rate, but the fact that it's reaccelerating after a slower period in FY2024. The sequential quarterly progression has been remarkably smooth: $759M → $789M → $811M → $836M. This kind of consistent step-up indicates a business where the pipeline is converting reliably, not lumpy deal-timing dependent.

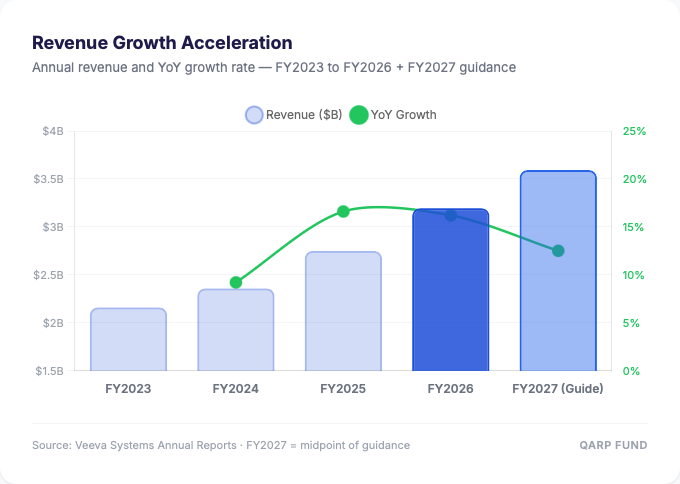

The Long Arc: From $2B to $6B

Looking at the multi-year picture, Veeva's revenue trajectory has gone from 9% growth in FY2024 to 16-17% in FY2025-2026, and the FY2027 guide implies 12% growth at the midpoint — with management reaffirming a $6 billion annual revenue target by FY2030. For context, FY2023 revenue was $2.16 billion. Getting to $6 billion in seven years requires a ~16% CAGR. The Vault CRM migration, new AI products, and geographic expansion are the levers to get there.

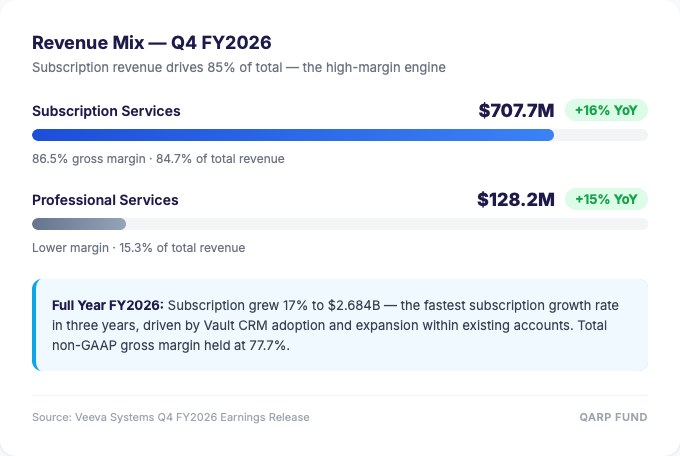

The Revenue Mix That Makes This Business Exceptional

Veeva's subscription revenue — $707.7 million in Q4, 84.7% of total — carries an 86.5% gross margin. That's an exceptional number in enterprise software. Professional services fills out the rest at 15%, lower-margin but important for implementation and expansion. The flywheel: every new Vault CRM or Vault Clinical customer drives professional services revenue during implementation, which then converts to recurring, high-margin subscription revenue for years. Full-year subscription revenue grew 17% — the fastest rate in three years.

FY2027 Guidance: Steady Acceleration

Management guided FY2027 to $3.585–$3.600 billion in revenue with non-GAAP EPS of approximately $8.85. That's +9% EPS growth on +12% revenue growth — implying some margin investment, likely in Veeva AI and international expansion. Q1 FY2027 is guided to $855–$858 million, which will be the first official data point showing whether Vault CRM momentum accelerates further into the new fiscal year.

What Wall Street Is Watching Now

Veeva has always been a company that earns its premium multiple through execution consistency. This quarter delivered that. The key question for the next 12 months: how fast does Vault CRM land the remaining top-20 biopharmas (currently 7 of 20 fully committed), and when does Veeva AI start showing up in ASP expansion? The answers will determine whether the stock re-rates further or consolidates near current levels.

Veeva reports Q1 FY2027 in June. Watch subscription revenue growth rate and Vault CRM live customer count for leading indicators of whether the FY2027 guidance proves conservative.