UnitedHealth Group (UNH): Healthcare Giant Navigating Challenges in 2025

The current valuation presents an attractive entry point for long-term investors willing to navigate near-term volatility.

Executive Summary

UnitedHealth Group faces a challenging 2025 after delivering strong 2024 results but experiencing unexpected medical cost pressures in Medicare Advantage. Despite generating over $400 billion in revenue in 2024, the company has revised its 2025 earnings guidance downward due to heightened care activity in its Medicare business. However, UNH's diversified business model through Optum continues to provide stability and growth opportunities.

Key Financial Highlights (2024)

Business Model Strength

UnitedHealth Group operates through two complementary segments:

UnitedHealthcare (~75% of revenue): Provides health benefits across commercial, Medicare, Medicaid, and international markets, serving over 53 million people globally.

Optum (~25% of revenue): Delivers healthcare services through three divisions:

Optum Health: Care delivery with ~105 billion in revenue

Optum Rx: Pharmacy benefits with over $130 billion in revenue

Optum Insight: Technology and analytics with $19 billion in revenue

Key Performance Metrics Analysis

Return on Invested Capital (ROIC)

UNH's ROIC declined to 8.0% in 2024 from 13.8% in 2023, primarily due to elevated medical costs and one-time impacts. Historically, the company has maintained strong ROIC above 13%, demonstrating efficient capital allocation.

Revenue Growth

The company achieved consistent revenue growth, with a 10-year CAGR of 9.7%. Revenue increased from $157.1B in 2015 to $400.3B in 2024, showcasing the company's market expansion and acquisition strategy.

Free Cash Flow Generation

Despite 2024 challenges, UNH generated $20.7B in free cash flow. The 10-year average FCF is approximately $16.8B, with peak generation of $25.7B in 2023.

Net Margins

Net margins compressed significantly in 2024 to 3.6% due to elevated medical costs in Medicare Advantage. Historical margins averaged around 5-6%, which management expects to restore as cost pressures normalize.

Debt Management

Net debt increased to $51.6B in 2024 ($76.9B total debt minus $25.3B cash). The debt-to-equity ratio of 77.3% reflects the company's leveraged growth strategy while maintaining investment-grade credit ratings.

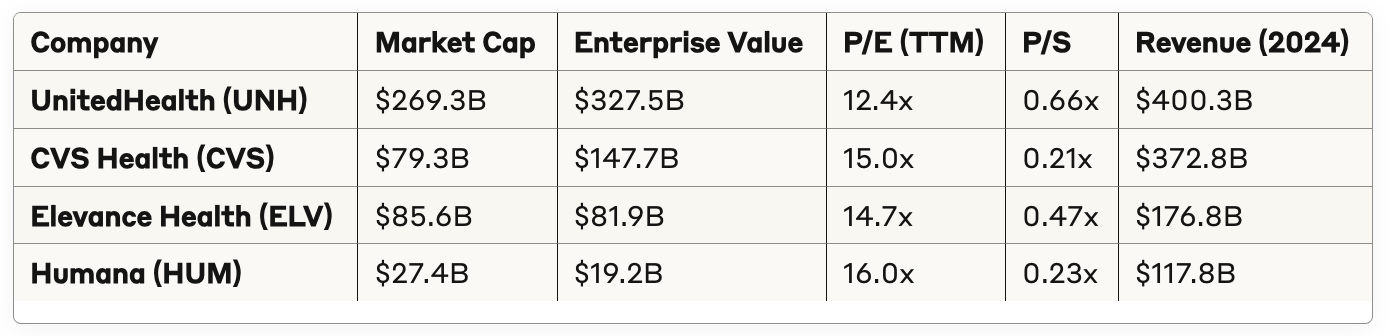

Valuation Analysis

Current Valuation Metrics

Peer Comparison

UNH trades at a discount to many peers despite its market leadership and diversified business model, suggesting potential value for long-term investors.

2025 Outlook and Challenges

Revised Guidance

Net Earnings: $24.65-$25.15 per share (down from $28.15-$28.65)

Adjusted Earnings: $26.00-$26.50 per share (down from $29.50-$30.00)

Revenue: $450-$455 billion

Operating Cash Flow: $32-$33 billion

Key Risk Factors

Medicare Advantage Pressures: Elevated medical costs and star rating challenges

Regulatory Oversight: Increased CMS auditing of Medicare Advantage contracts

Competition: Market share pressure from other major insurers

Cyber Security: Ongoing costs from 2024 Change Healthcare cyberattack

Growth Opportunities

Medicare Advantage Market Share: Potential to gain members as competitors struggle

Optum Expansion: Continued growth in care delivery and technology services

Commercial Insurance: Strong growth in self-funded employer plans

International Markets: Expansion opportunities in global healthcare services

Investment Thesis

Bull Case

Market Leadership: Dominant position in Medicare Advantage with scale advantages

Diversified Revenue: Optum provides stability and higher-margin growth

Cash Generation: Strong FCF supports dividend growth and share buybacks

Valuation Opportunity: Stock trades at attractive multiples relative to historical norms

Competitive Moat: Integrated healthcare model difficult to replicate

Bear Case

Medicare Headwinds: Ongoing pressure from CMS rate updates and star ratings

Medical Cost Inflation: Rising healthcare costs pressuring margins

Regulatory Risk: Potential for increased government intervention

Execution Risk: Challenge of integrating Optum acquisitions and delivering synergies

Technical Analysis

The stock has declined from highs near $550 in 2023 to current levels around $311, representing a significant correction. Key support levels exist around $300, while resistance is at $350-$375. The dividend yield of 2.8% provides downside support for income-focused investors.

Conclusion

UnitedHealth Group remains the undisputed leader in U.S. healthcare, with an unmatched scale and diversified business model through Optum. While 2025 presents near-term challenges in Medicare Advantage, the company's long-term fundamentals remain strong.

The current valuation presents an attractive entry point for long-term investors willing to navigate near-term volatility. UNH's ability to generate substantial free cash flow, maintain market leadership, and expand through Optum positions it well for long-term value creation despite current headwinds.

Rating: BUY

Price Target: $380-$420 (12-month)

Risk Level: Moderate

Investors should monitor quarterly results for evidence of Medicare cost stabilization and Optum growth acceleration.

Disclaimer: This analysis is for informational and educational purposes only and should not be considered as personalized investment advice.