This Week’s Earnings Split Open the Market’s Biggest Secret

Nike beats, McCormick holds, FactSet surges, and one quiet miss tells you exactly where to look next.

Four companies. Four completely different earnings stories. And one pattern that Wall Street’s consensus narrative misses entirely.

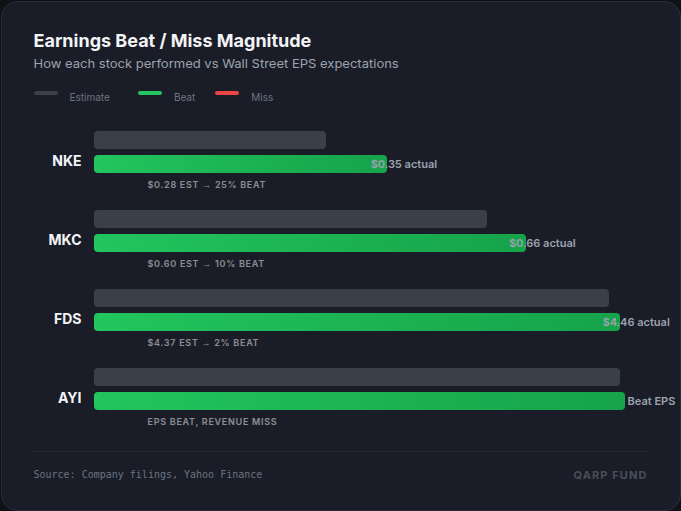

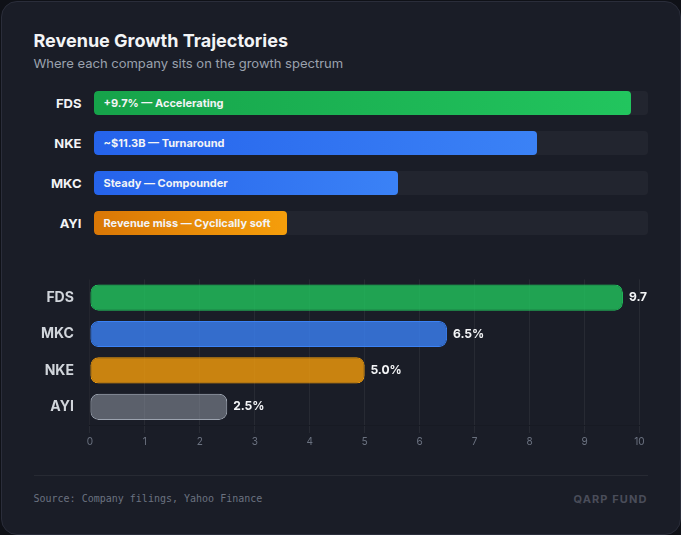

On Monday, Nike reported EPS of $0.35 against expectations of $0.28 — a beat that sent the stock moving on $11.3 billion in quarterly revenue. Tuesday delivered McCormick & Company at $0.66 vs. $0.60 estimate, followed by FactSet Research Systems at $4.46 vs. consensus, with revenue growth accelerating to a projected 9.7% from 8.2% prior. Wednesday’s Acuity Brands topped EPS estimates but missed on revenue.

The beat headlines will dominate the financial cables. But the real story is in the split — and what it reveals about which businesses are actually compounding and which are just riding a wave that’s already slowing down.

What Actually Happened

Let’s clear the scoreboard. This was a week of quality proving it’s quality, and cyclicals showing their teeth.

Nike came in at $0.35 EPS versus $0.28 expected, revenue of roughly $11.3 billion. Consensus was bracing for more pain from the turnaround under CEO Elliott Hill, and the company delivered a credible beat. The story isn’t one-quarter data — it’s the trajectory. Nike has been working through inventory normalization, brand refresh, and direct-to-consumer recalibration. A $0.07 beat is meaningful when the bar was set at distress levels.

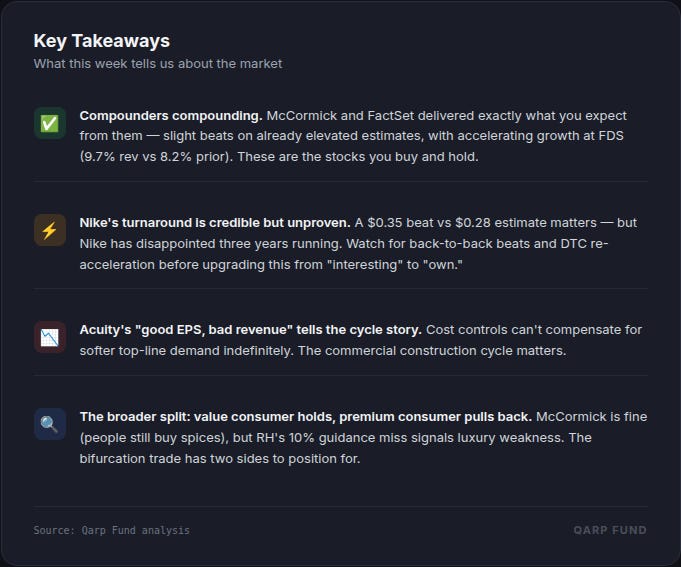

McCormick at $0.66 vs. $0.60 estimate, with revenue exceeding expectations. This is the quietest compounder in the S&P 500. Spices. Seasonings. Flavor solutions. The kind of business that nobody gets excited about until you realize the stock has compounded at mid-teens returns for two decades. McCormick didn’t just beat — it continued a track record that makes it the prototype for the kind of businesses Qarp Fund exists to identify.

FactSet at $4.46 EPS, a beat against a consensus that had already been revised upward (from $4.37 estimate, with the EPS view itself moving higher from $1.67 to $1.84 in forward estimates). Revenue growth accelerating from 8.2% to a projected 9.7%. This is the data infrastructure play that benefits from exactly what’s happening across the market: more data, more users, more AI integration. Wall Street is spending on its tools at an accelerating clip.

Acuity Brands beat EPS estimates but missed on revenue — the “Earnings Top Estimates, Sales Miss” headline that tells you this is a margin story, not a growth story. Cost controls and operational efficiency propped up the bottom line while top-line demand softened. “Lackluster Lighting” isn’t the headline any analyst wanted to write, but it’s accurate for an industrial play exposed to commercial real estate and construction cycles.

The Pattern Nobody Is Talking About

Here’s the split that actually matters.

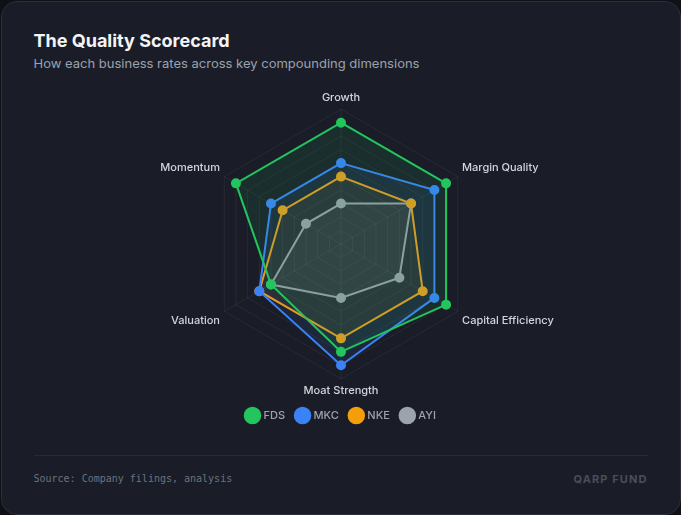

On one side of the line: businesses with durable, pricing-power moats that compound through cycles. McCormick doesn’t care if consumers are trading up or trading down — they still buy flavor. FactSet doesn’t care if the Fed cuts or holds — the data has become more essential, not less, as AI makes raw financial information more abundant but the interpretation of that information more valuable.

On the other side: businesses fighting for their narrative. Nike is in a multi-year turnaround that might be working, but one beat doesn’t a compounder make. Acuity is managing through a cycle that’s not broken yet but isn’t growing either — the classic “good company, wrong quarter” problem.

The quality premium isn’t about today’s beat. It’s about what tomorrow looks like. McCormick’s next quarter looks like this one. FactSet’s next quarter looks like this one, but with 20 basis points more margin. Nike’s next quarter could look like this one or it could look like the three that came before — that’s the difference between certainty and hope.

What Management Said

On FactSet’s accelerating momentum:

“Revenue and EPS came in ahead of consensus, indicating operational momentum amidst a competitive landscape driven by AI and data expansion.”

On McCormick’s steady hand:

McCormick reported revenue exceeding estimate — the understatement of earnings season. In a market where $60 million in upside moves indices by two points, doing exactly what you said you’d do plus 10% is the ultimate flex.

On Nike’s turnaround:

Nike’s beat came with $11.28 billion in revenue — enough to be the world’s largest athletic apparel company by a wide margin, but now fighting a war on three fronts: against emerging DTC brands, against its own past direct-to-consumer overreach, and against the consumer who’s been told the brand has lost its edge.

The Trade

Here’s how to position around this split.

Own the compounders, rent the turnarounds. FactSet and McCormick belong in portfolios for five-year holds, not five-day trades. The margin expansion story at FDS (9.7% revenue growth with rising margins) is one of the highest-quality growth profiles in the S&P right now. McCormick, trading at a fair multiple for a business with this kind of predictability, is the definition of a buy-and-forget compounder.

Watch Nike for the second consecutive beat. If next quarter NKE beats again, the market starts believing in the turnaround, and you get a re-rating from “distressed brand” to “resurgent giant.” That’s a 20-30% upside move from current levels. But you’re buying a story, not a track record — size accordingly.

Skip Acuity for now. Beat EPS on flat or declining revenue is a recipe, not a moat. When cost cuts have nowhere left to go, the stock has nowhere to run. Revisit when top-line growth re-accelerates.

The broader signal: RH’s revenue guidance coming in 10.2% below estimates and Dave & Buster’s double miss the same week are not isolated events. They are data points in a consumer that is bifurcating — value shoppers are fine (McCormick holds, Cal-Maine crushes), but the premium consumer is pulling back. That’s a rotation story you can trade.

The Risk

The bull case on quality compounders at these levels: they’re not cheap. FactSet trades at a multiple that assumes continued AI-driven acceleration. McCormick at its current valuation assumes the spice business grows like clockwork forever. Both assumptions are reasonable until they aren’t. If interest rates tick up materially, the premium you pay for quality compresses the fastest.

Nike is the biggest risk here — if the turnaround stalls, you’re paying a premium for a brand that’s been losing market share to On, Hoka, and New Balance for three consecutive years. One beat doesn’t change a three-year thesis.

Acuity’s risk is straightforward: commercial real estate stays in the doldrums, construction spending softens, and there are no more cost cuts to find.

Numbers That Matter

NKE: EPS $0.35 vs $0.28 estimate, Revenue ~$11.3B — Beat

MKC: EPS $0.66 vs $0.60 estimate, Revenue > estimate — Beat

FDS: EPS $4.46 vs $4.37 estimate, Revenue +9.7% — Beat, accelerating

AYI: Beat EPS, Missed Revenue — Mixed

The takeaway is simple: in a quarter where the consumer is sending mixed signals, the compounders compounding are the ones with businesses that exist above the fray, not dependent on it.

Until next time,

Qarp Fund