The Membership Machine Runs At Full Speed: Costco's Q2 Earnings Show Digital Resilience and Pricing Power

Costco Beat on Both Earnings and Revenue, Yet Market Remains Skeptical

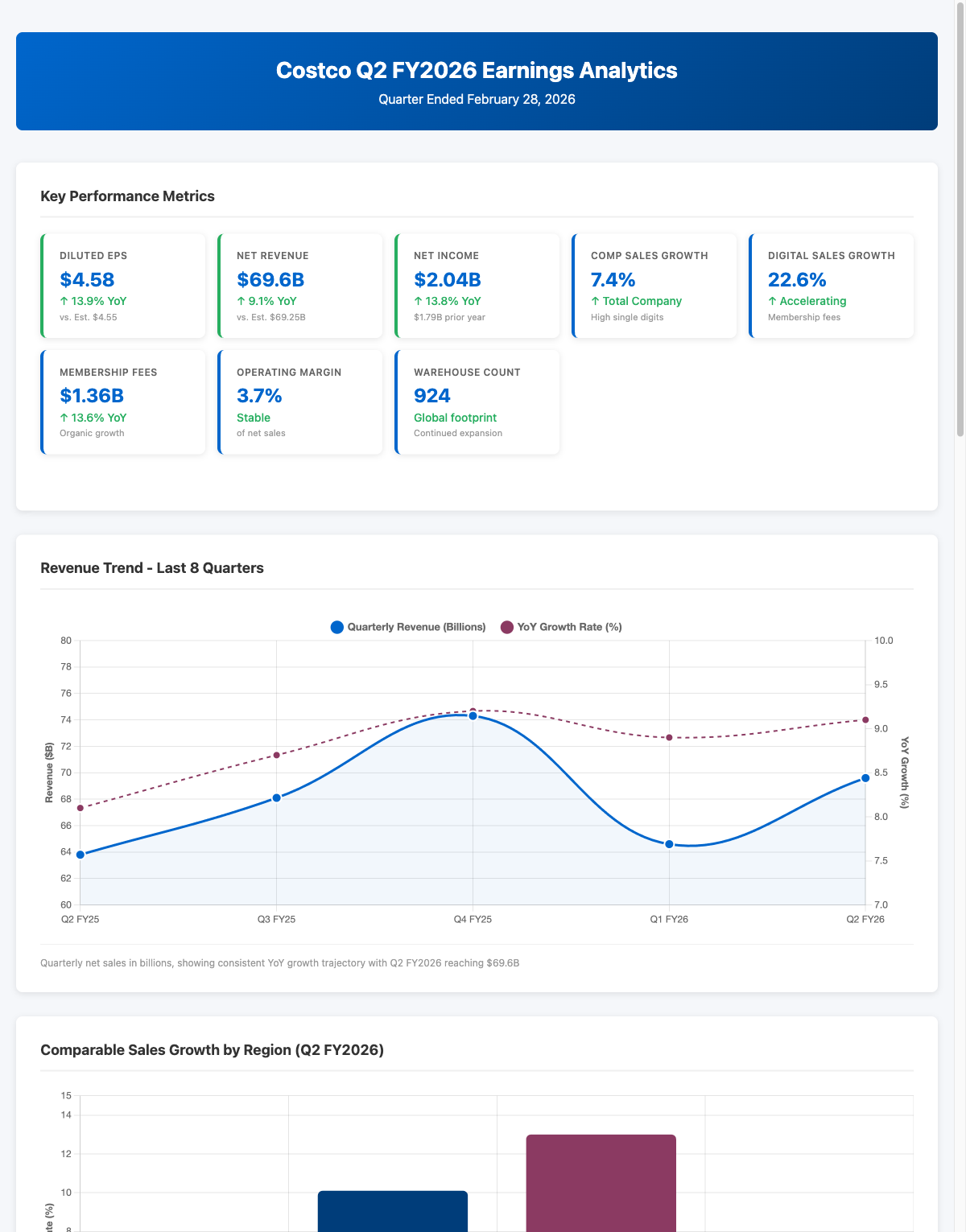

Costco Wholesale (COST) reported second-quarter fiscal 2026 results that exceeded Wall Street expectations on both the headline metrics and the operational fundamentals that matter most to investors. The warehouse giant reported diluted earnings per share of $4.58, beating consensus estimates of $4.55, with total net revenue reaching $69.6 billion, topping the Street's $69.25 billion estimate. Net income surged 13.8% year-over-year to $2.04 billion. Yet despite this clean beat on both fronts, the market's initial reaction was dismissive—shares declined 2.4% in after-hours trading, a reminder that even executing perfectly isn't always rewarded when valuation expectations run this high

.

The Real Story: Membership and Digital Are Accelerating

What matters most in Costco's results isn't the $0.03 beat on EPS or the $350 million revenue beat. It's the underlying momentum in the business model that makes Costco arguably the most resilient consumer-facing company in America today.

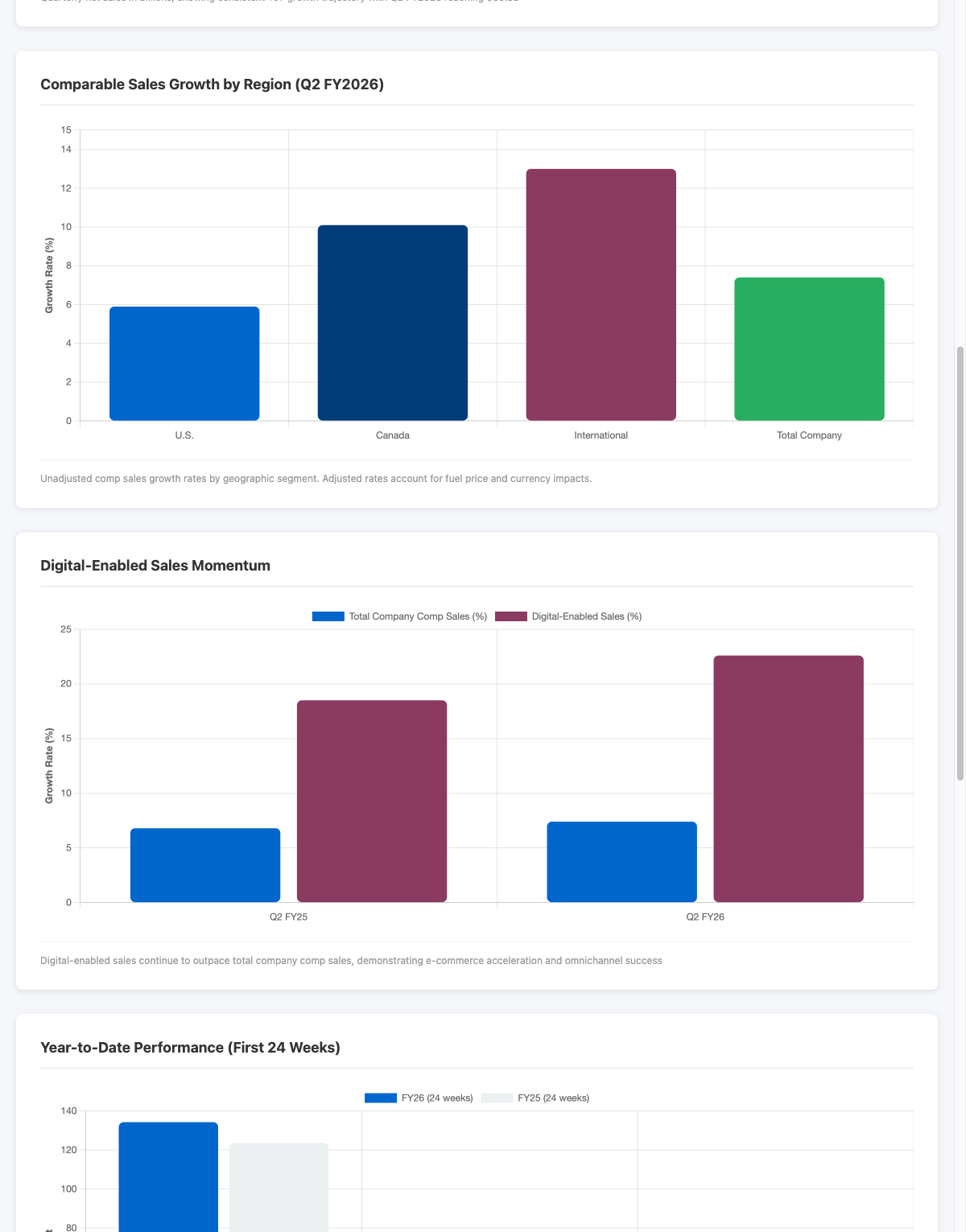

Comparable sales growth of 7.4% may sound pedestrian in isolation, but the regional breakdown tells a much more interesting story. U.S. comp sales advanced 5.9% (adjusted 6.4%), while Canada powered ahead with 10.1% growth, and the International segment posted 13.0% comp sales growth. These aren't warehouse club numbers—these are high-single-digit growth rates across every major geography, suggesting that Costco's value proposition remains sticky regardless of macro conditions.

But the real growth engine is digital. Digital-enabled sales surged 22.6% in the quarter, now representing a material portion of the company's transaction volume. This is critical context: Costco isn't growing faster because it's lowering prices or cutting margins to defend share. It's growing faster because members are using Costco in more ways—visiting warehouses, ordering online, mixing physical and digital experiences. That omnichannel capability is exactly what's powering the 13.9% year-over-year EPS growth.

Membership: The Billion-Dollar Recurring Revenue Stream

Costco's real profit engine isn't selling groceries or televisions—it's selling memberships. In the quarter, membership fee income hit $1.36 billion, up 13.6% year-over-year. That's a recurring revenue stream growing faster than the company's core retail business, with better economics than selling physical goods.

Think about what that means: Costco added enough net new members and saw enough upgrades to Executive memberships to drive that fee revenue growth in a mature market. This isn't a growth story borrowed from emerging markets or new geographies—this is a story of deepening penetration in a saturated domestic market, with members voting with their wallets that the membership is worth renewing

.

Operating Leverage and Margin Stability

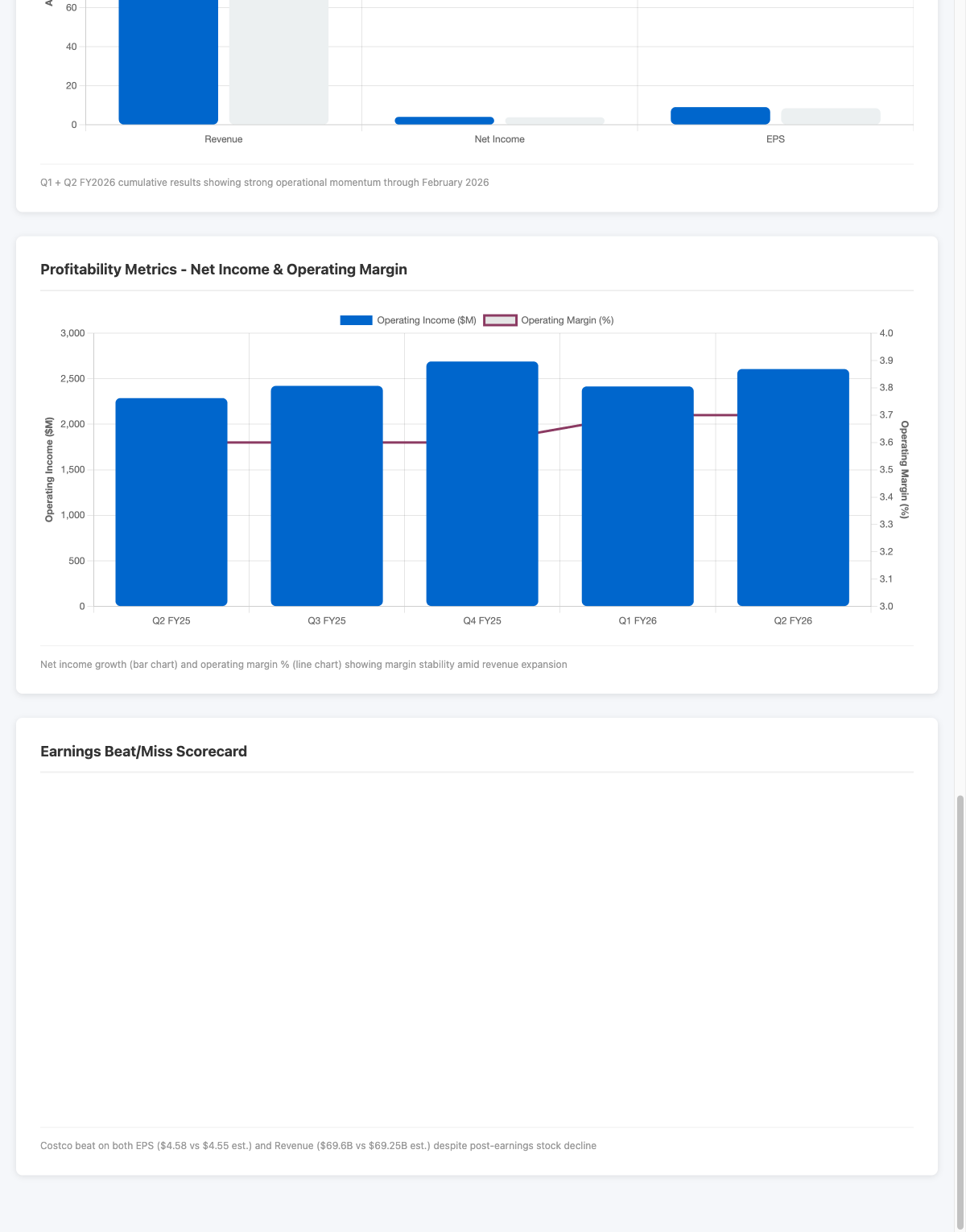

One of the most overlooked aspects of Costco's business is operating margin stability. In Q2, the company maintained 3.7% operating margins despite revenue growing at 9.1% year-over-year. This isn't a company squeezing margins to make the numbers; it's a company that has optimized its cost structure so thoroughly that it can invest in digital, expand its footprint to 924 warehouses worldwide, and still deliver steady profitability.

The operating income picture reinforces this: Q2 operating income of $2.61 billion is up from $2.29 billion in the prior year quarter—an 13.8% increase that matches the EPS growth rate. Costco's entire value chain—from sourcing to logistics to warehouse operations—is functioning at a high level of efficiency.

The Warehouse Count Matters More Than You Think

Costco now operates 924 warehouses worldwide, with 634 in the U.S. and Puerto Rico, 114 in Canada, 42 in Mexico, and 37 in Japan. In a capital-intensive business, the company has been disciplined about expansion, opening only where unit economics pencil out. The fact that it's maintaining strong same-store sales while expanding the base suggests that new warehouse openings are filling white space rather than cannibalizing existing locations.

Through the first 24 weeks of fiscal 2026, Costco deployed $2.82 billion in capital expenditures while generating $7.68 billion in operating cash flow. That's a positive working capital story that gives management confidence to continue reinvesting in the business.

Why The Stock Sold Off (And Why That Might Be Wrong)

COST is trading at an elevated valuation multiple—the market has been pricing in perfect execution for years. A beat on earnings, while good, isn't shocking for a company that's been executing consistently. The stock's post-earnings decline reflects not disappointment in Costco's results, but rather the reality that the bar for a positive surprise has been set very high.

However, there's something important in these results that markets might be underappreciating: the resilience of the membership base during a period of macro uncertainty. The 13.6% growth in membership fee revenue happened in the same economy where consumer credit is at stress levels and some retailers are guiding down. That Costco is adding members and pushing more of them into the higher-margin Executive tier suggests that the business has untapped pricing power.

Looking Forward

Costco doesn't provide forward guidance, but the trends embedded in these results are clear. Digital acceleration is driving higher attachment rates without compromising warehouse economics. Geographic diversification is reducing dependence on U.S. comps. Membership fee growth is outpacing merchandise sales growth, indicating a shift towards higher-quality, stickier revenue.

The market will likely remain skeptical of COST's valuation until the macro environment shows more explicit signs of strength. But in a world where consumer resilience is suspect and execution risk is everywhere, Costco's ability to grow comps in the high single digits while expanding membership fee revenue and maintaining operating margin stability is increasingly rare and increasingly valuable.

For investors focused on quality of earnings, consistency of execution, and recession-resistant revenue streams, the membership machine is still the best story in retail.