The AI Pivot Is Working. Wix Closes 2025 on a High Note.

Q4 revenue of $524M (+14% YoY), EPS of $1.81 crushing estimates by 23%, and Base44 hitting $100M ARR in nine months — Wix's AI bet is already paying off.

Wix just reported its best earnings quarter in two years — not because of a revenue blowout, but because of what's happening underneath the surface. EPS came in at $1.81, a 23% beat against consensus. Base44, the AI-native website builder Wix acquired nine months ago, has already hit $100M in ARR. And the company is simultaneously raising $250M and buying back $2B of its own stock. That's a lot of conviction in one earnings report.

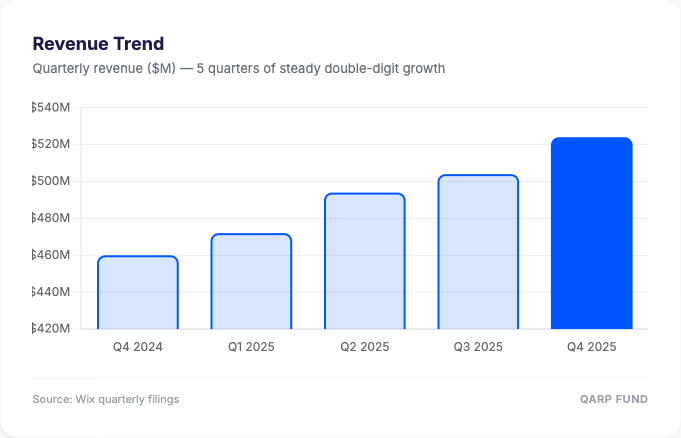

📊 Revenue Keeps Compounding

Wix grew revenue 14% year-over-year to $524M in Q4, capping a full year at $1.99B — up 13% for 2025. That's steady, not spectacular. But the bookings picture is more encouraging: total Q4 bookings hit $535M (+15% YoY), and ARR reached $1.84B, also up 14%.

The revenue trend matters here. Five straight quarters of double-digit growth, with Q4 2025 marking the strongest in the streak at $524M — up from $460M a year ago.

🏗️ Partners Is the Fastest Engine

The segment breakdown tells the real story of Wix's transformation. For full-year 2025:

Creative Subscriptions: $1.41B (+11% YoY) — the core SMB business, steady

Partners: $750M (+23% YoY) — agencies and freelancers building on Wix

Business Solutions: $583M (+18% YoY) — payments, bookings, ecommerce tools

Transactions: $255M (+19% YoY) — take-rate on commerce flowing through the platform

The Partners segment growing at 23% — nearly twice the rate of core subscriptions — signals a structural shift. Wix is becoming a platform businesses build on, not just a tool individuals use. That changes the retention profile, the contract size, and the long-term monetization ceiling.

🎯 EPS Beat Was the Headline

Revenue came in essentially in line with expectations ($524M vs. $527M estimated). But the real beat was on profitability:

Non-GAAP EPS: $1.81 vs. $1.47 estimated — a 23% beat

Adjusted Operating Income: $81M vs. $77M estimated — beat by 6%, 15.5% margin

Free Cash Flow: $156M in Q4, $573M for the full year — 30% FCF margin

This is a company with improving operating leverage. Revenue growing at 13-14% while EPS and FCF grow faster means the margin story is intact even as Wix invests heavily in AI.

🔮 2026 Outlook: Confident, Not Cautious

Management's 2026 guidance was straightforward: mid-teens revenue and bookings growth across both Q1 and the full year. FCF margin guided to the "low-to-mid 20% range" — a step down from the 30% delivered in 2025, reflecting accelerated AI investment.

The strategic numbers are more interesting than the guidance range:

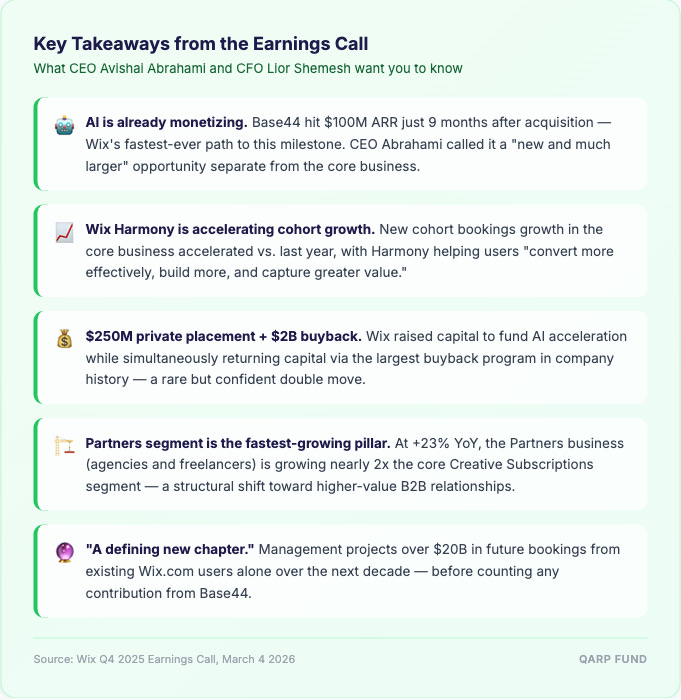

Base44 ARR: $100M — reached nine months after acquisition. CEO Abrahami explicitly called this a "new and much larger" opportunity separate from the core Wix.com business

$2B share buyback authorized — the largest in company history, majority to be completed by end of 2026

$250M private placement — led by Durable Capital Partners, capital earmarked to accelerate AI development

$20B+ in future bookings projected from existing Wix.com users over the next decade, before any Base44 contribution

⚡ The Bottom Line

What does this quarter actually signal? Wix is threading a needle most software companies can't: deploying capital into AI while simultaneously returning capital to shareholders. The $250M raise + $2B buyback combo isn't contradictory — it's a statement that management believes the AI investments will generate returns that justify both.

The risk is execution. Wix Harmony and Base44 are bets that AI-native creation tools become the default for website builders over the next 3-5 years. If that plays out, the $20B future bookings projection starts to look conservative. If AI commoditizes website creation entirely, Wix's core subscription business faces structural headwinds.

For now, the numbers say the bet is working.

Until next time,

Qarp Fund