Netflix (NFLX): The Streaming Giant's Path to $1 Trillion Market Cap

TL;DR: Netflix delivered exceptional Q1 2025 results with 13% revenue growth and expanding margins. The company's shift from subscriber growth to revenue focus, combined with accelerating advertising revenue and strong content performance, positions it well for sustained growth despite intensifying competition.

Executive Summary

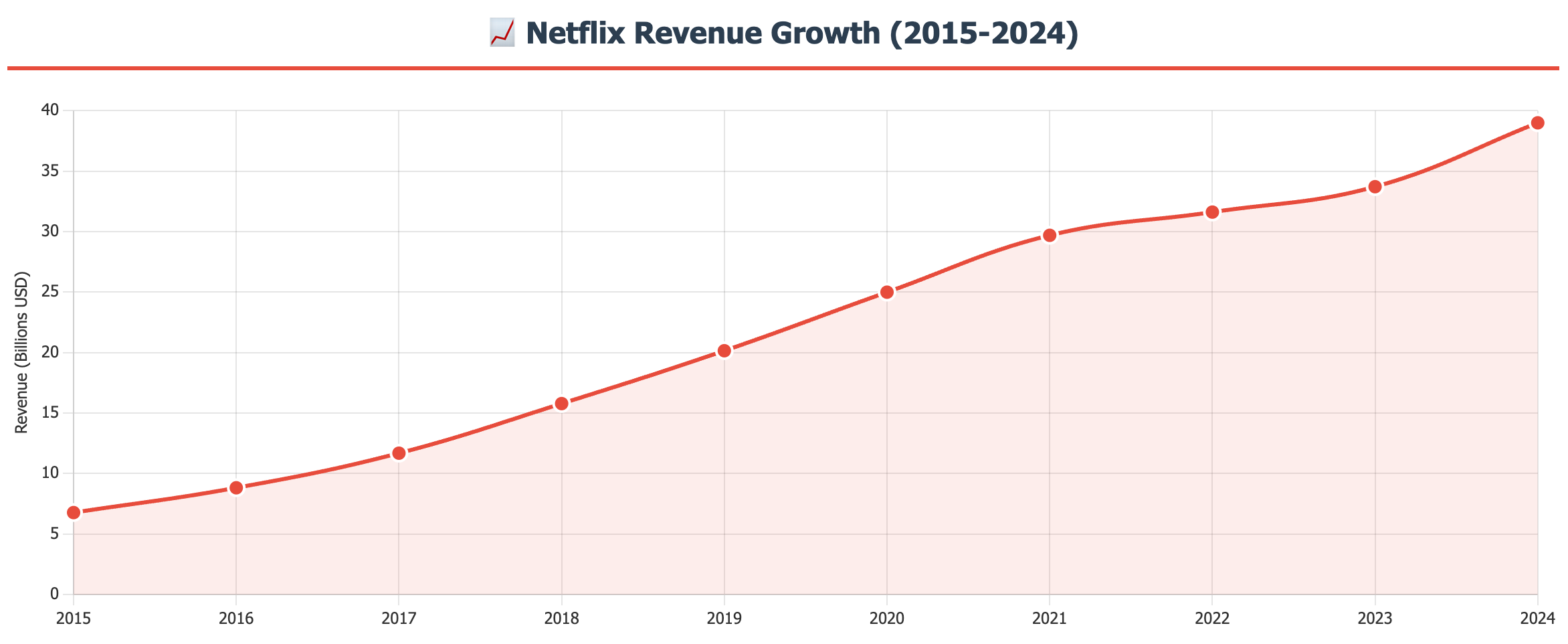

Netflix continues to dominate the streaming landscape, but its strategy has fundamentally evolved. No longer the pure growth story of the 2010s, Netflix has transformed into a mature, profit-generating machine with ambitious plans to double its $39 billion revenue by 2030 and reach a $1 trillion market capitalization.

Key Investment Highlights:

Revenue Growth: 13% YoY growth in Q1 2025 to $10.54 billion

Profitability: Operating margin expanded to 31.7%, rivaling tech giants

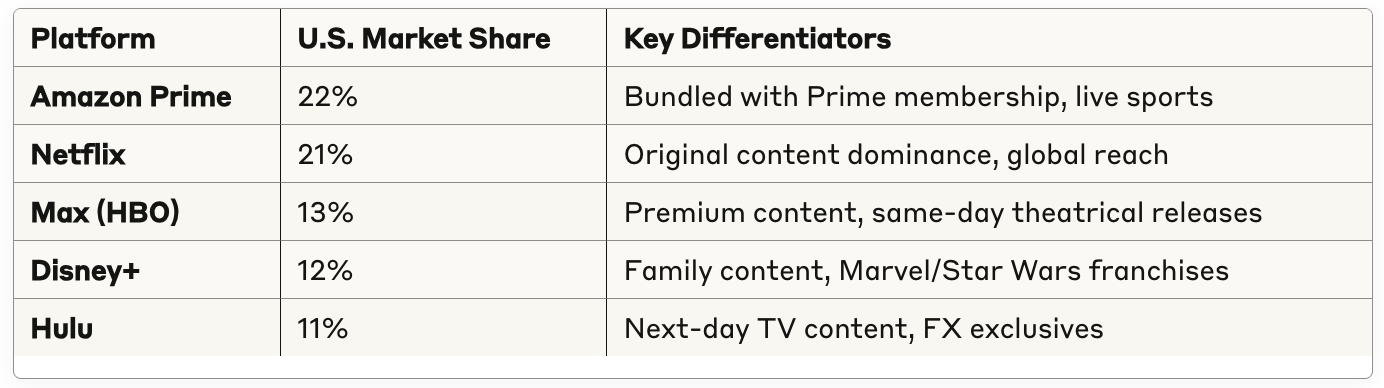

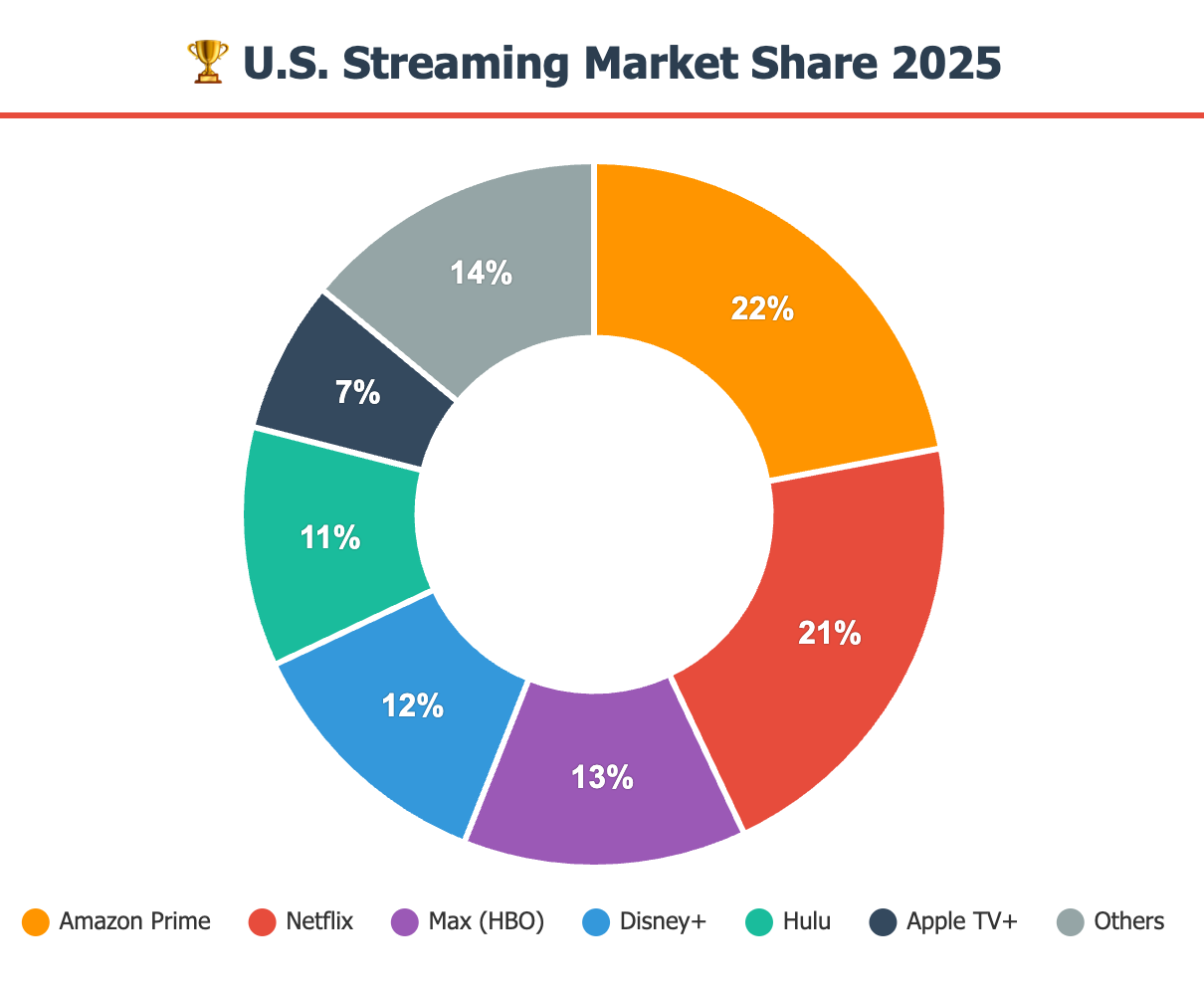

Market Position: 21% U.S. market share, competing neck-and-neck with Amazon Prime

Strategic Pivot: Focus shifted from subscriber counts to revenue and engagement metrics

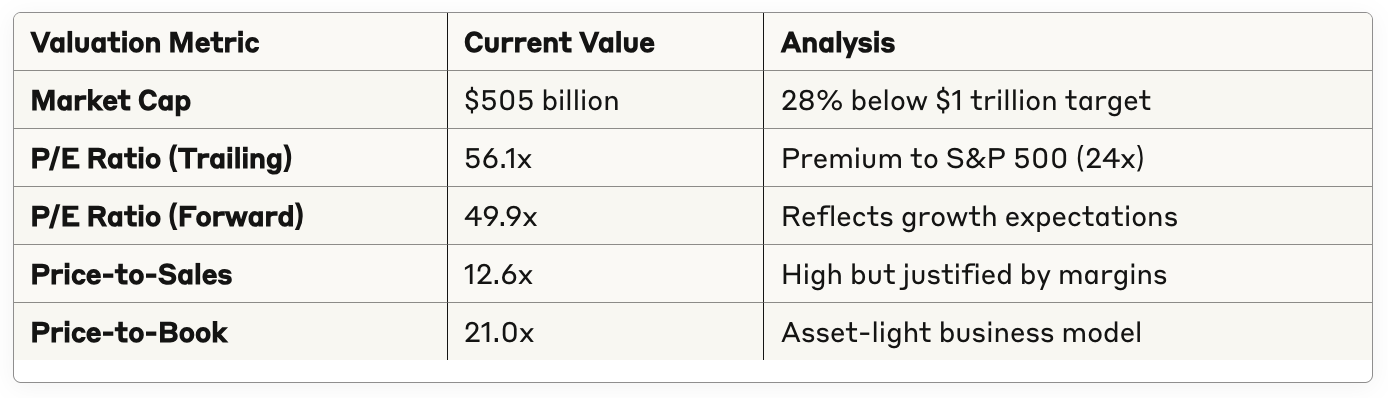

Current Valuation: $505 billion market cap, trading at 56x trailing P/E

Financial Performance: A Profit Powerhouse

Revenue Trajectory and Margin Expansion

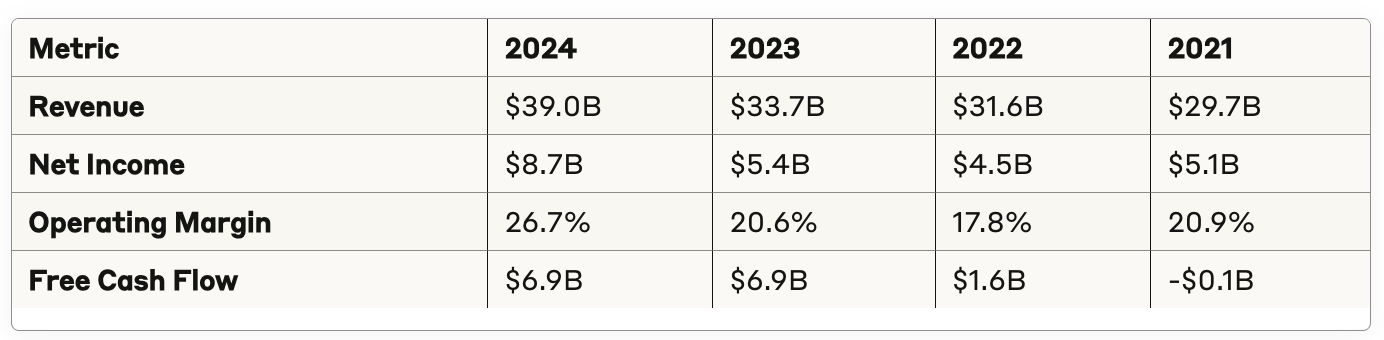

Netflix's financial evolution tells a compelling story of maturation. After years of prioritizing growth over profitability, the company has achieved remarkable margin expansion while maintaining double-digit revenue growth.

The Q1 2025 results showcased this transformation:

Revenue: $10.54 billion (+13% YoY) vs. $10.52 billion expected

EPS: $6.61 vs. $5.71 expected

Operating Margin: 31.7% vs. 28.1% in Q1 2024

Free Cash Flow: $2.66 billion

Netflix's operating margin of 31.7% is almost unheard of in media, more in line with companies like Apple or Google than Netflix's streaming peers.

The End of Subscriber Obsession

Netflix made a strategic decision to stop disclosing subscriber counts quarterly, wanting to focus the narrative on financials and user engagement. This shift reflects the company's evolution from a growth-at-all-costs startup to a mature media enterprise focused on sustainable profitability.

Why This Matters:

Allows Netflix to focus on revenue quality rather than quantity

Reduces quarterly volatility from subscriber misses

Aligns with long-term value creation strategy

Market Position and Competition

Streaming Wars: A Two-Horse Race

The streaming landscape has consolidated into a battle between Netflix and Amazon Prime Video for market leadership:

Amazon Prime Video leads the U.S. streaming market, holding a 22% share, while Netflix remains a close competitor with 21%. However, Netflix actually has the true majority of market share as subscribers use the platform solely for its content, unlike Prime Video which is bundled with Amazon's broader ecosystem.

Competitive Advantages

Content Moat: Netflix's content library represents its strongest competitive advantage. In 2022, original and exclusive content on Netflix accounts for over 50% of titles in the US catalog, an increase from the 20.6% share in March 2019.

Global Scale: Netflix reaches 700 million people worldwide, providing unmatched global distribution for content investments.

Conversion Excellence: Netflix has a conversion rate of 93%, which is higher than that of Amazon Prime.

Growth Drivers and Strategic Initiatives

1. Advertising: The Next Revenue Frontier

Netflix's advertising tier represents a massive opportunity for revenue diversification:

Current Status: Netflix has 70 million global ad-supported subscribers

Growth Trajectory: Co-CEO Greg Peters said Netflix expects to double its advertising revenue this year

Market Penetration: In countries where it shows ads, the ad plan accounted for 50% of the new membership sign-ups in the quarter

Strategic Advantages:

In-house ad tech platform launched in April 2025

Programmatic capabilities planned for 2026

Live events driving higher ad rates

2. Live Programming and Sports

Netflix's expansion into live content marks a significant strategic shift:

WWE Partnership: Exclusive "Monday Night Raw" streaming since January 2025

NFL Content: Christmas Day games returning in 2025

Sports Strategy: Live events command premium advertising rates and reduce churn

3. Gaming and Interactive Content

While currently a negligible revenue contributor, gaming represents a long-term growth opportunity:

Expanding mobile gaming portfolio

Interactive content experimentation

Potential for new monetization models

4. Price Optimization

Netflix's pricing power remains strong despite competitive pressure:

Recent Increases: January 2025 price hikes across all tiers

Premium Tier: $24.99 (up from $22.99)

Ad-Supported: $7.99 (up from $6.99)

Low Churn: Price increases absorbed with minimal subscriber loss

Valuation Analysis

Current Metrics

Analyst Targets and Outlook

Wall Street sentiment remains constructive with mixed optimism:

Consensus Target: $1,136.51 per share (current: $1,240.55)

Range: $720 - $1,514 per share

Bull Case: Pivotal Research raised target to $1,350 (Street high)

Bear Case: Some analysts cite slowing subscriber growth concerns

24/7 Wall St. projects Netflix stock will slip to $1,080.00 per share by year's end, based on continued, triple-digit growth in advertising revenue and high-double-digit ad plan subscriber growth.

Path to $1 Trillion

Netflix executives reportedly said their goal is to double the company's $39 billion in revenue last year by 2030 and reach a market capitalization of $1 trillion.

Requirements for $1T Market Cap:

Current market cap: $505 billion

Required gain: ~98%

Implied stock price: ~$2,400

Revenue target: $78 billion by 2030

Risk Factors and Challenges

Competitive Pressures

Intensifying Competition: Increased competition from services like Disney+, Amazon Prime, and Apple TV+ puts pressure on Netflix to retain subscribers and differentiate itself with unique content.

Content Costs: Rising talent costs and production expenses pressure margins despite scale advantages.

Market Saturation

Mature Markets: North American subscriber growth is slowing as market penetration increases.

Economic Sensitivity: While historically resilient, streaming faces pressure during economic downturns.

Execution Risks

Technology Transitions: Ad tech platform rollout must execute flawlessly to capture advertising opportunity.

Live Content: Sports and live programming require different operational capabilities.

Investment Thesis

Bull Case

Margin Expansion: Operating margins approaching 32% with further upside potential

Advertising Acceleration: Doubling ad revenue annually from growing base

Global Growth: Continued international expansion, particularly in emerging markets

Content Moat: Unmatched original content library driving engagement and pricing power

Capital Efficiency: Strong free cash flow generation enabling shareholder returns

Bear Case

Valuation Concerns: 56x P/E ratio offers limited margin of safety

Competition Intensity: Market share pressure from well-funded rivals

Growth Deceleration: Slowing subscriber growth in mature markets

Economic Sensitivity: Consumer discretionary spending vulnerable to recession

Conclusion: A Mature Growth Story

Netflix has successfully navigated the transition from disruptive growth company to profitable media giant. The company's strategic shift from subscriber obsession to revenue focus reflects this maturation and positions it well for sustained long-term growth.

Key Takeaways:

Financial Excellence: Best-in-class margins and cash generation

Strategic Evolution: Successful pivot to advertising and live content

Market Leadership: Maintaining competitive position despite intensified rivalry

Ambitious Targets: $1 trillion market cap goal appears achievable but challenging

Investment Recommendation: Netflix represents a quality growth story trading at a premium valuation. The company's execution track record, competitive moat, and multiple growth drivers support continued outperformance, though investors should expect volatility and potentially more modest returns given the current valuation.

For investors seeking exposure to the streaming revolution with a proven winner, Netflix remains the gold standard despite its premium price.

Disclaimer: This analysis is for informational purposes only and should not be considered personalized investment advice. Always conduct your own research and consult with financial professionals before making investment decisions.