Key Takeaways from MSCI's Q1 2025 Earnings

The latest earnings report for MSCI ($MSCI) for Q1 2025 shows strong growth and healthy profits. Here are the top 10 things you need to know, explained in simple terms.

1. Core Revenues Drive Strong Growth

MSCI’s main business is doing very well.

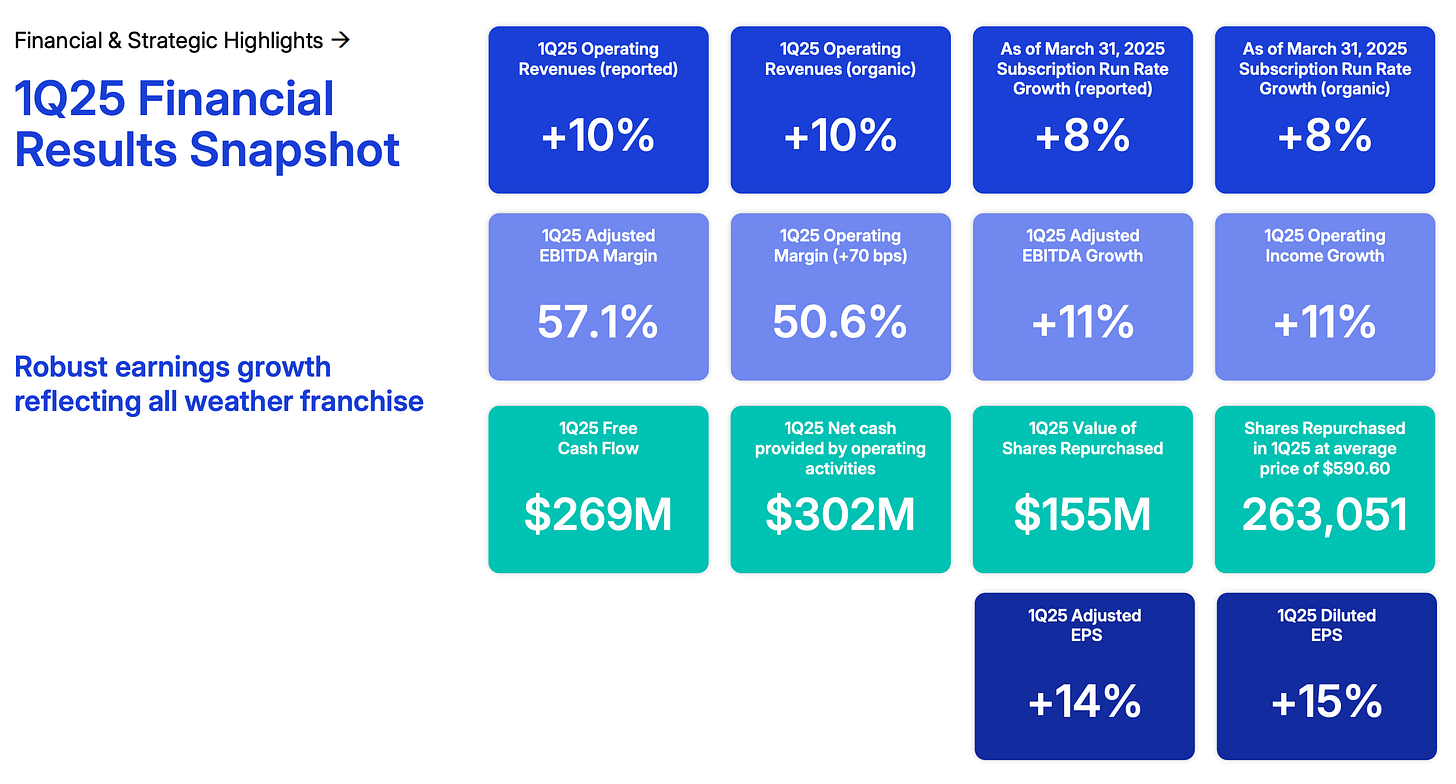

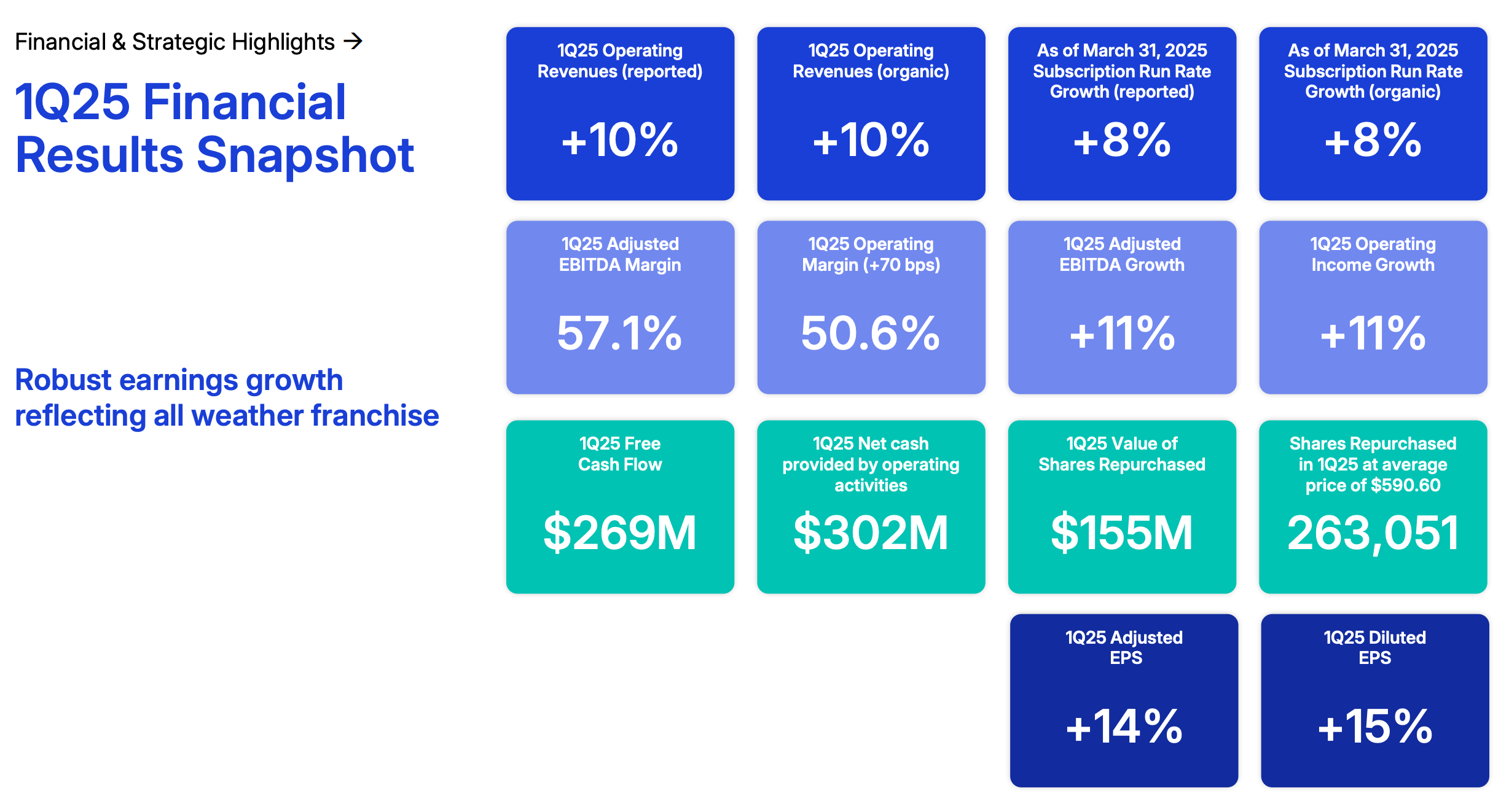

Record Revenues: The company earned $745.8 million in the first quarter of 2025. That’s a 9.7% increase from last year.

Organic Growth: Revenue from MSCI’s own business (without buying new companies) grew 9.9%.

High Demand: More customers are using MSCI’s tools and services to make investment decisions.

What This Means: Almost 10% growth shows MSCI’s main products are popular and trusted, putting the company in a great position for the rest of the year.

2. Recurring Revenues Bring Stability

MSCI’s subscription services keep money coming in.

Steady Growth: Recurring subscription revenues went up 7.7%.

Bigger Subscription Base: The subscription “run rate” increased by $175 million, meaning more customers are signing up or staying.

Organic Subscription Growth: Organic recurring subscription run rate rose 8.2%.

Why It Matters: Recurring revenues make MSCI’s income more predictable and help the company stay steady, even if other parts of the business change.

3. Asset-Based Fees Are Rising Fast

MSCI earns more money as people invest in its funds.

Big Increase: Asset-based fees jumped by 18.1% compared to last year.

Fee Run Rate Up: The run rate for these fees grew by $77.8 million.

More Investments: This is because more money is put into funds that use MSCI’s indexes.

Why It Matters: Strong growth here means MSCI’s products are popular with investors and could keep earning more if the trend continues.

4. Profits and Margins Are Very Strong

MSCI is earning more from every dollar it makes.

Operating Margin: MSCI kept 50.6% of its revenue as profit after costs.

Adjusted EBITDA Margin: Even higher at 57.1%, showing great cash earnings from the main business.

Adjusted EBITDA Up: This important profit measure grew 11% to $425.6 million.

Operating Income Up: Operating income rose 11.1% to $377.0 million.

Why This Matters: High margins and growing profits are signs that MSCI manages its money well, which is good news for investors.

5. Earnings Per Share (EPS) Continue to Climb

Each share of MSCI stock is now worth more.

Net Income Up: MSCI made $288.6 million in profit, a 12.8% increase from last year.

Diluted EPS: EPS rose 15.2% to $3.71 per share.

Adjusted EPS: Adjusted EPS reached $4.00, up 13.6%.

Why This Matters: Higher EPS means more value for shareholders and shows the company is turning sales into real profit.

6. Index Segment Leads the Way

MSCI’s Index business is its top performer.

Index Revenues Up: This segment grew 12.8% to $421.7 million.

Subscriptions and Fees Up: Recurring subscriptions rose 9.6%, and asset-based fees jumped 18.1%.

Index Run Rate: Expected yearly revenue from the Index business climbed 10.5% to $1.6 billion.

Other Segments Growing Too:

Analytics: Up 5.0% to $172.2 million

Sustainability and Climate: Up 8.6% to $84.6 million

Private Assets: Up 4.7% to $67.3 million

Tip: The Index segment is the biggest driver, but all parts of MSCI are growing.

7. Client Retention and Run Rate Are Strong

MSCI keeps almost all of its clients.

High Retention: The client retention rate is 95.3%—up from 92.8% last year.

Run Rate Up: Yearly income expected from clients reached $2.98 billion, a 9.3% increase.

Why This Matters: Loyal clients and steady income help MSCI plan for the future and stay strong.

8. Dividends, Buybacks, and Cash

MSCI takes care of its shareholders.

Dividends Paid: Shareholders received $139.7 million in dividends this quarter.

New Dividend Announced: A $1.80 per share cash dividend is coming for Q2 2025.

Share Buybacks: MSCI bought back 493,322 shares for $275.4 million.

Cash on Hand: The company has $360.7 million in cash.

Tip: These actions show MSCI is rewarding its shareholders and staying financially healthy.

9. Cash Flow and Investments

MSCI manages its money carefully.

Net Cash from Operations: MSCI brought in $301.7 million, a 0.5% increase from last year.

Free Cash Flow: Ended at $268.9 million, down 2.5%.

Investments: Spent $32.9 million on new equipment and upgrades this quarter.

Plans for the Year: MSCI expects to invest $115–$125 million in 2025 to support future growth.

10. Positive Outlook for the Rest of the Year

MSCI expects more growth ahead.

Operating Expenses: Will be between $1.405–$1.445 billion for the year.

Adjusted EBITDA Expenses: Expected to be $1.22–$1.25 billion.

Strong Cash Flow: MSCI expects $1.525–$1.575 billion in net cash from operations, and $1.4–$1.46 billion in free cash flow.

More Employees: MSCI now has 6,184 employees, a 5.6% increase.

Tip: These strong forecasts show MSCI is confident about growth and is investing in people and new projects.

Final Thoughts

MSCI’s latest earnings report is packed with good news: higher revenues, strong profits, loyal customers, and big plans for the future. Whether you’re an investor or just interested in the company, these results show MSCI is in a great place for 2025 and beyond.