Key Takeaways from Moody's Q1 2025 Earnings Report

Moody’s ($MCO) just released its 1Q25 earnings report, and there’s a lot for investors to be excited about. Here are the seven most important things you should know from this quarter’s results.

1. Strong Revenue Growth Across the Board

Moody’s had a great start to 2025 with impressive revenue numbers:

Total revenue reached $1.9 billion, up 8% from last year.

This shows Moody’s business is growing and getting stronger.Both main divisions did well:

Moody’s Analytics (MA) made $859 million, up 8% year-over-year.

Moody’s Investors Service (MIS) earned $1.1 billion, also up 8%.

Record-setting quarters, even with currency challenges.

Even though changes in foreign currency slightly hurt results (about 1%), both divisions still had record or near-record quarters.

What this means for investors:

Steady growth across all parts of the business shows Moody’s is on a healthy path. Even when things get tough, the company keeps moving forward.

2. Recurring Revenue Leads the Way at MA

Moody’s Analytics (MA) is building its business on steady, reliable income:

Recurring revenue is huge:

MA’s annualized recurring revenue (ARR) hit $3.3 billion, up 9% from last year.96% of MA’s revenue is recurring.

Almost all the money MA makes comes from subscriptions and ongoing services, not one-time sales. This makes MA’s income stable and predictable.All segments are growing:

Decision Solutions grew the fastest, up 11%.

Research & Insights rose 6%.

Data & Information increased 3%.

Why this matters:

Recurring revenue acts like a safety net. With steady income, MA can handle tough times and plan for the future—good news for investors.

3. Record Results in Ratings, Even During Market Ups and Downs

Moody’s Investors Service (MIS) had a standout quarter:

MIS reached its highest quarterly revenue ever.

Even when markets are unpredictable, MIS’s ratings business stays strong.Transactional revenue grew 8%.

More companies turned to Moody’s for ratings on new deals and bonds.Structured finance revenue soared 21%.

This big jump was driven by more refinancing in products like CLOs and CMBS.Not all areas grew:

Revenue from rating financial institutions dropped 2%, mostly because insurance companies issued fewer bonds.

Tip for investors:

Watch for trends in transactional and structured finance revenues—they give hints about where the market is going.

4. Earnings Per Share and Margins on the Rise

Moody’s is earning more money for each share and becoming more efficient:

Earnings per share (EPS) jumped:

Diluted EPS rose to $3.46, up 10%.

Adjusted diluted EPS reached $3.83, up 14%.

Operating margins are improving:

Overall margin was 44.0%.

Adjusted margin hit 51.7%, up 1 percentage point from last year.

Both divisions are more efficient:

MA’s adjusted margin rose to 30.0%.

MIS set a new high with a 66.0% adjusted margin.

What this means:

Moody’s is making more profit from every dollar it earns—a strong sign of a healthy business.

5. Smart Cost Management While Still Investing

Moody’s is spending more, but doing it wisely:

Operating expenses rose 9% to $1.08 billion.

This is mostly due to higher pay, key investments, costs from recent mergers, and some restructuring.Expense growth will slow down.

For the rest of 2025, Moody’s expects only a small increase in expenses.Balancing investment and savings:

The company is working to spend smartly—investing in growth but also looking for ways to save money.

Bottom line:

Moody’s is focused on growing its business, but not at the expense of profits.

6. Strong Cash Flows and Rewards for Shareholders

Moody’s is generating a lot of cash and sharing it with investors:

Operating cash flow was $757 million, and free cash flow was $672 million.

This means the company has plenty of money to run its business and pay investors.Higher dividends:

Moody’s raised its dividend by 11% to $0.94 per share.Continued share buybacks:

The company bought back 0.8 million shares at $481.77 each, and still has $1.2 billion left for more buybacks.Debt is under control:

With $6.8 billion in debt, Moody’s uses its strong cash flow to manage payments and stay on solid ground.

Why this matters:

Strong cash flow, higher dividends, and buybacks show Moody’s cares about rewarding its shareholders.

7. Looking Ahead: Cautious Optimism and a Focus on Subscriptions

Moody’s is planning for steady growth, even if the economy is slow:

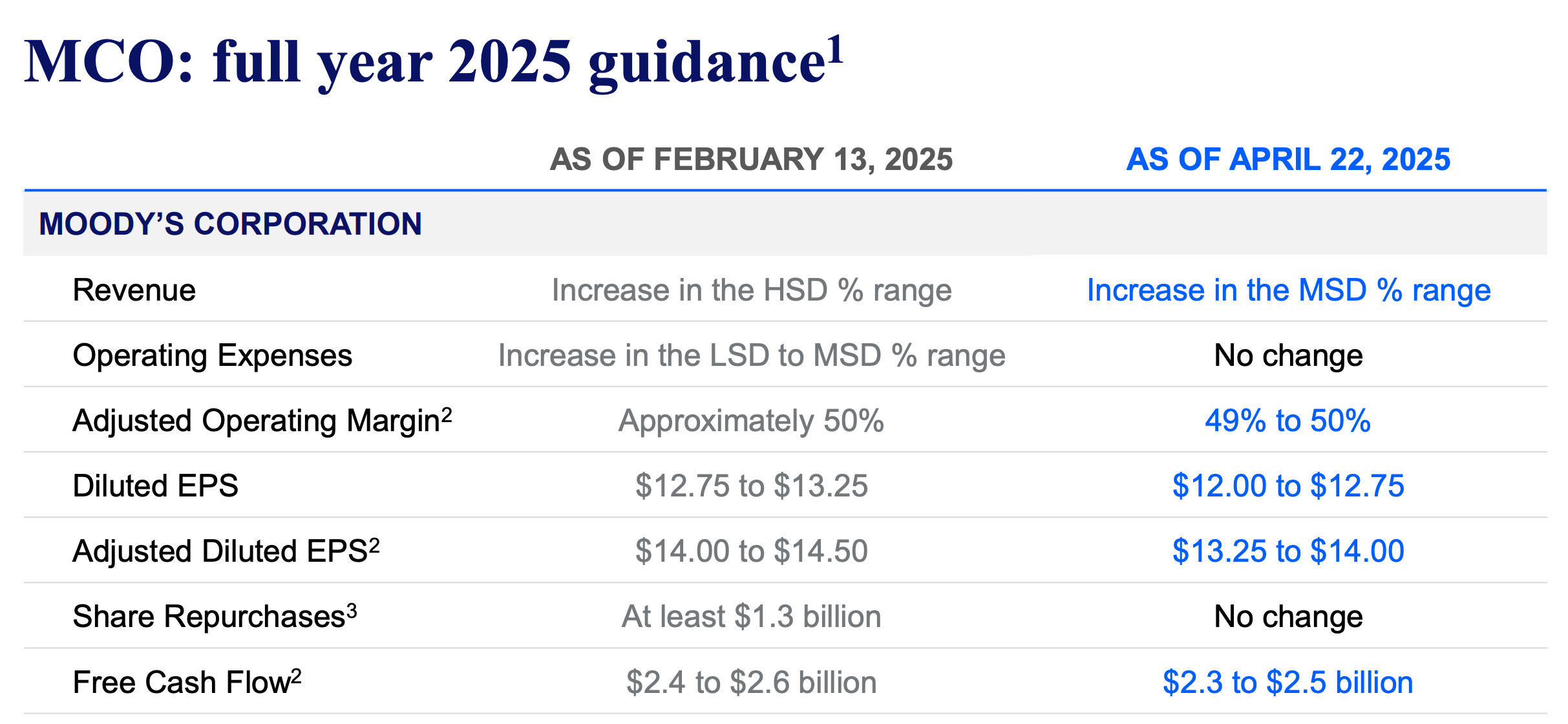

Raised earnings guidance:

Moody’s now expects full-year 2025 EPS to be $12.00–$12.75 and adjusted EPS to be $13.25–$14.00—about a 9% increase from last year.Expecting slow economic growth:

The company thinks U.S. GDP will grow just 0–1%, and global GDP 1–2% in 2025.Inflation will stay high:

U.S. inflation is expected to stay between 3.5% and 4.5%.Focus on subscriptions:

MA’s transactional revenue (one-time sales) dropped 21% in Q1.

Moody’s is growing its subscription-based services, making revenue steadier and more reliable.

What this means for investors:

Even with a slow economy and higher prices, Moody’s is confident it can keep growing by focusing on steady, recurring income.

Final Thoughts

Moody’s 1Q25 earnings show strong growth, smart management, and a focus on rewarding shareholders. With steady recurring revenue, rising profits, and a flexible strategy, Moody’s is on a solid path—even when the economic future looks uncertain.

If you’re an investor looking for a stable and growing company, Moody’s continues to deliver.