I Analyzed 82 Superinvestor Portfolios. Here's What They're All Buying.

Every quarter, the world’s best investors quietly file their 13-Fs. I parsed all 82 of them so you don’t have to.

March 2026 • Q4 2025 13-F Analysis • 82 portfolios • ~$2 trillion in AUM

There’s a game the smartest money managers in the world play every quarter. They’re required by law to disclose their U.S. equity positions 45 days after each quarter ends. By the time retail investors read about it, the institutions are often already three moves ahead.

But here’s what most people miss: the signal isn’t in any single manager’s portfolio — it’s in the overlap.

When 16 different superinvestors all add to the same stock in the same quarter, that’s not coincidence. When 6 of the world’s best fund managers all open brand new positions in the same company simultaneously, that’s a coordinated moment of conviction worth paying attention to.

I scraped and analyzed all 82 superinvestor portfolios tracked by Dataroma — managers like Warren Buffett, Bill Ackman, David Tepper, Seth Klarman, Chase Coleman, and 77 others — and identified every buy and add from Q4 2025. Here’s what they’re telling us.

The Methodology (Quick Version)

Source: Dataroma.com — 82 portfolios tracked, Q4 2025 13-F filings

Scope: Every “Buy” (new position) and “Add” (position increase) event

Total: 844 stocks with buy or add activity identified

Distinction that matters: A “New Buy” means the manager opened a fresh position they didn’t hold before. An “Add” means they already owned it and bought more. Both are bullish, but new buys signal higher conviction.

Current prices as of early March 2026

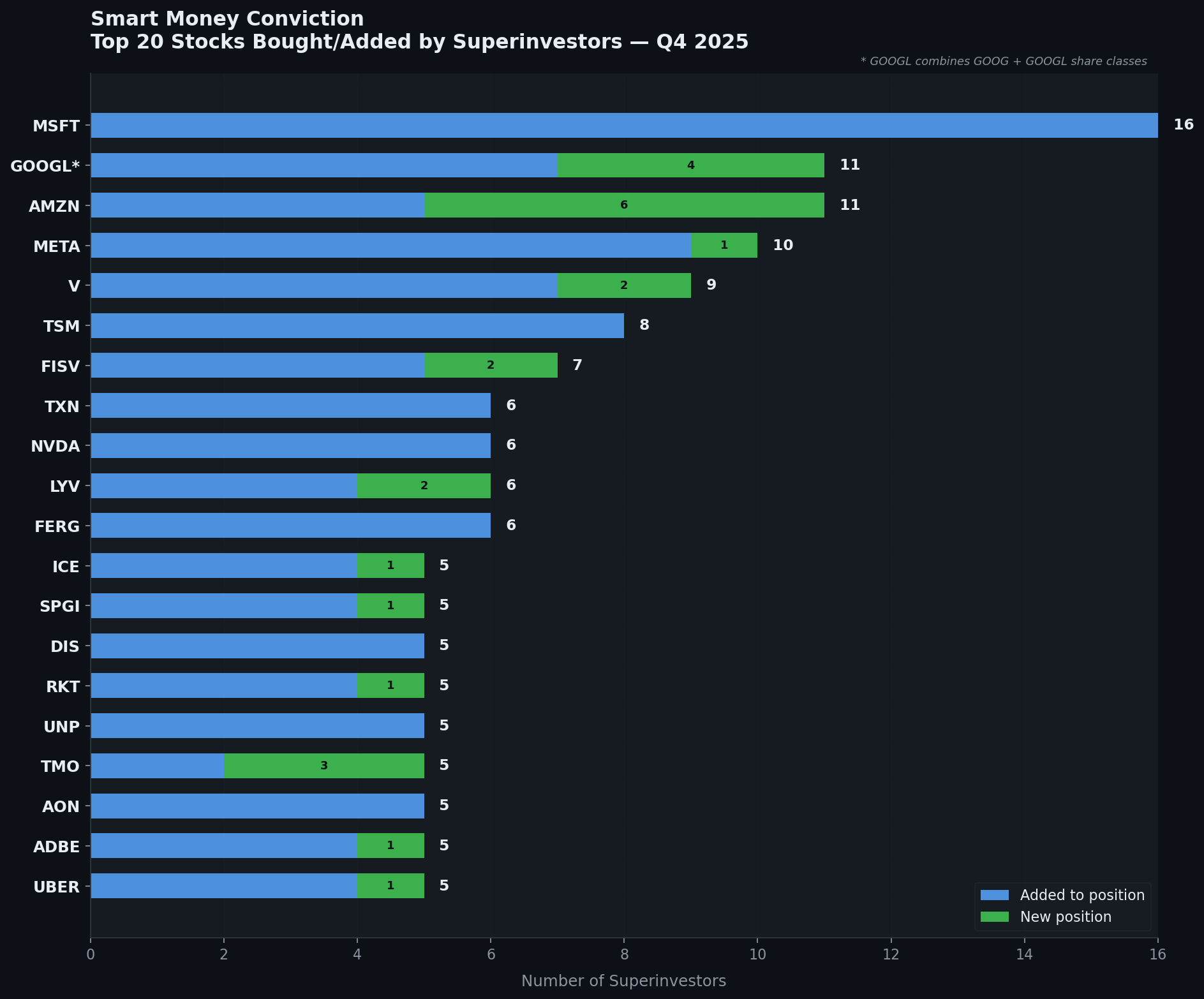

Chart 1: The Full Conviction Ranking

Green = New position opened. Blue = Existing position increased. Number inside green = count of new buys.

The Four Pillars of the Consensus Trade

1. Microsoft (MSFT) — 16 Investors Added. Zero Opened Fresh.

Microsoft is the most-added stock in the dataset by a wide margin. 16 separate superinvestors added to their MSFT positions in Q4 2025. That’s not a coincidence — that’s a coordinated recognition that the stock had gotten cheap enough to act on.

Here’s the twist: not a single one of those 16 opened a new position. Every one of them already owned it. What they did was buy more.

The numbers tell you why. Microsoft hit a 52-week high of $552 in mid-2024. By Q4 2025, it had pulled back to the mid-$400s — a roughly 25% drawdown in one of the most enduring compounding machines in the market. Azure cloud growth continues to accelerate, Copilot AI monetization is beginning to show up in enterprise contracts, and the company generates roughly $80 billion in free cash flow annually.

Among those adding: Chris Hohn’s TCI Fund, David Tepper, Stephen Mandel’s Lone Pine, Thomas Gayner, William Von Mueffling’s Cantillon Capital, Duan Yongping (the legendary Chinese value investor), and Francois Rochon — a geographically diverse group with wildly different investing styles, all arriving at the same conclusion.

Current price: $408.96 | 52-week range: $342 – $552 | Where it sits in range: Bottom third | Since Q4 filing: -15.4%

The stock has actually continued declining since the Q4 filing date. 16 managers thought it was cheap at ~$475. At $409, it’s even cheaper. The market is offering you a better price than they got.

2. Amazon (AMZN) — The Biggest Fresh Conviction Signal

If MSFT is the consensus add, Amazon is the consensus new buy — and that’s the more powerful signal.

6 superinvestors opened brand new Amazon positions in Q4 2025: David Rolfe (Wedgewood Partners), Dennis Hong (ShawSpring), Jensen Investment Management, Seth Klarman (Baupost Group), Thomas Russo, and Viking Global Investors. Five more added to existing positions.

That’s 11 total buy events, with more than half representing fresh capital deployment from managers who hadn’t previously held it (or hadn’t held it recently).

Why now? A few things converged in Q4 2025: AWS re-accelerated to 19% growth and is now running at an annualized $115B+ revenue rate; Amazon’s advertising business hit $60B+ for the year; and margins expanded dramatically as the company shifted from “build at all costs” back to “optimize and harvest.” The stock had also pulled back meaningfully from its 2024 highs.

Seth Klarman opening a new position is particularly notable. Baupost is known for deep value and special situations — not mega-cap tech. When Klarman buys Amazon, he’s saying the margin of safety has become compelling.

Current price: $213.21 | 52-week range: $161 – $259 | Where it sits in range: Middle | Since Q4 filing: -7.6%

3. Meta Platforms (META) — The AI Revenue Machine

10 managers bought or added Meta in Q4 2025, making it the third-most-acted-upon stock. Nine added to existing positions; Bill Ackman opened a new one.

Meta is increasingly the simplest AI investment thesis on the market: the company spent $40B+ on AI capex and is seeing direct revenue returns through ad targeting improvements. Instagram Reels is monetizing at YouTube-level rates. WhatsApp Business is barely scratched. And at roughly 22x forward earnings, it’s not expensive for a business growing revenue 20%+ with 40%+ margins.

Ackman’s new position is worth flagging. He’s now running a concentrated 11-stock portfolio and just added META as a top 5 position at around $660 per share. It’s now trading at $645 — modestly below his entry.

Current price: $644.86 | 52-week range: $479 – $795 | Since Q4 filing: -2.3%

4. Alphabet (GOOG + GOOGL) — 11 Investors, Two Share Classes

Combining both share classes, 11 distinct superinvestors bought or added Alphabet in Q4 2025 — the largest unique-investor count after MSFT and AMZN. Four opened fresh positions.

The Alphabet thesis is simple and powerful: the company is being valued as if AI kills Google Search. It won’t. Google Search is deeply embedded, generates ~$200B in annual revenue, and Google’s own AI (Gemini) is advancing rapidly. Meanwhile, YouTube is growing, Waymo is making real commercial progress, and Google Cloud is re-accelerating.

Christopher Davis, Francois Rochon, Harry Burn, William Von Mueffling, and Christopher Bloomstran all added significantly. Viking Global and two others opened new positions.

Current price: $298.52 | 52-week range: $140 – $349 | Where it sits in range: Upper third | Since Q4 filing: -4.6%

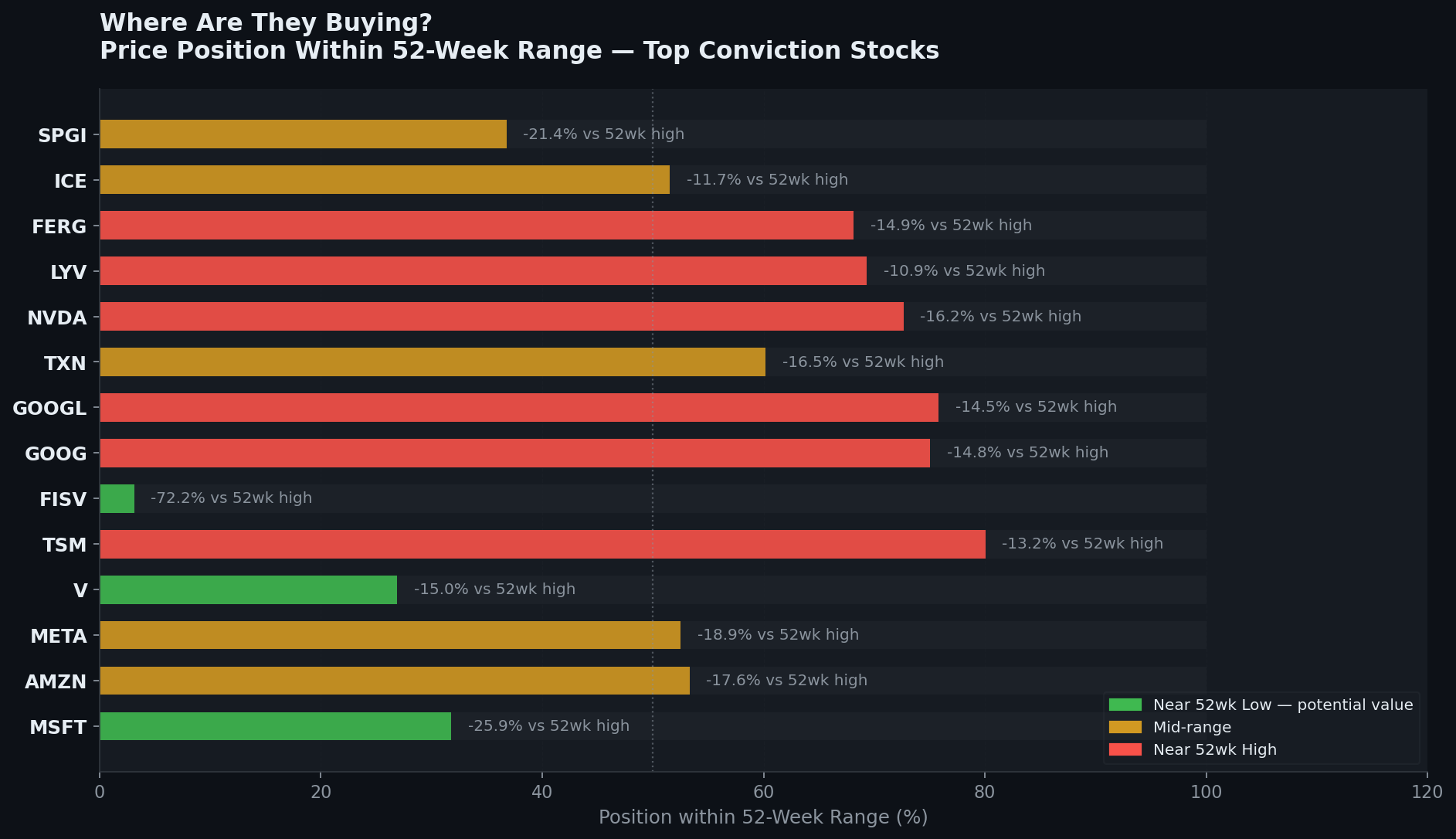

Chart 2: Where Are They Buying? (52-Week Range Positioning)

The further left a bar, the closer to the 52-week low — meaning superinvestors are buying at relatively cheap prices. Green = near lows. Red = near highs.

This chart is where the real opportunity analysis lives.

The Value Quadrant: High Conviction + Near 52-Week Lows

These are the stocks where smart money is buying and the price is near the low end of its annual range — suggesting you can get in at prices close to or better than what these managers paid.

Visa (V) — 9 Investors, Near-Bottom Range

9 superinvestors bought or added Visa in Q4 2025 — the fourth-highest in the dataset. More importantly, the stock is currently sitting at just 27% of its 52-week range, meaning it’s near its annual lows.

The bear case on Visa is always some variation of “fintech will displace it.” It hasn’t. Visa processes over $15 trillion in annual payment volume and has a virtually unassailable network effect. Two investors (AKO Capital and Stephen Mandel) opened fresh positions while seven others added.

At $317, Visa is -15% from its 52-week high of $373 and has pulled back -9.5% since the Q4 filing. You’re getting this at lower prices than the managers who filed.

Current price: $317.36 | 52-week range: $297 – $373 | Where it sits: 27% (near lows) | Since Q4 filing: -9.5%

Adobe (ADBE) — Near 52-Week Lows, 5 Managers Buying

Adobe is the most beaten-down quality name in the top conviction list. At $283, the stock is sitting at just 19% of its 52-week range — near its annual floor — and is -37% from its 52-week high of $452.

Five managers acted in Q4: Dodge & Cox, Lee Ainslie, Lindsell Train, Robert Olstein, and William Von Mueffling. One opened a fresh position.

The AI fear narrative (that generative image tools will make Adobe obsolete) has been priced in aggressively. But Adobe’s creative suite and PDF monopoly have proven remarkably sticky. The company is integrating AI into its products (Adobe Firefly) and continues to grow revenue at high single digits. At ~22x forward earnings, this is historical value territory for a business with 30%+ operating margins.

Current price: $283.62 | 52-week range: $244 – $452 | Where it sits: 19% (near lows) | Since Q4 filing: -19.0%

ADBE has continued to sell off since the Q4 filing. Five managers were buying it ~25% higher. You now have the opportunity to buy quality at a price they couldn’t.

Copart (CPRT) — 4 Managers, Near Annual Lows

Copart often flies under the radar because it operates in an unsexy business (salvage auto auctions), but it compounds like a dream — 20%+ ROE, asset-light, network effects, and no debt.

Four managers added in Q4 (AKO Capital, Chuck Akre, Torray Funds, Yacktman), and the stock is sitting at just 13% of its 52-week range — nearly at its annual floor.

If you want a high-quality compounder near 52-week lows with institutional backing, Copart deserves a spot on your watchlist.

Current price: $37.74 | 52-week range: $32 – $46 | Where it sits: 13% (near lows)

S&P Global (SPGI) — Duopoly Power at a Discount

5 managers bought or added SPGI including Chris Hohn, Glenn Greenberg, and Lindsell Train. The stock is -21% from its 52-week high and at 37% of its annual range.

SPGI and Moody’s are the world’s rating agency duopoly. They also own the S&P 500 index (Visa-like network effects on passive investment flows) and IHS Markit data. This is a toll-road business with irreplaceable infrastructure. It’s rarely cheap. Right now, it’s approaching cheap.

Current price: $452.36 | 52-week range: $381 – $576 | Where it sits: 37% | Since Q4 filing: -13.4%

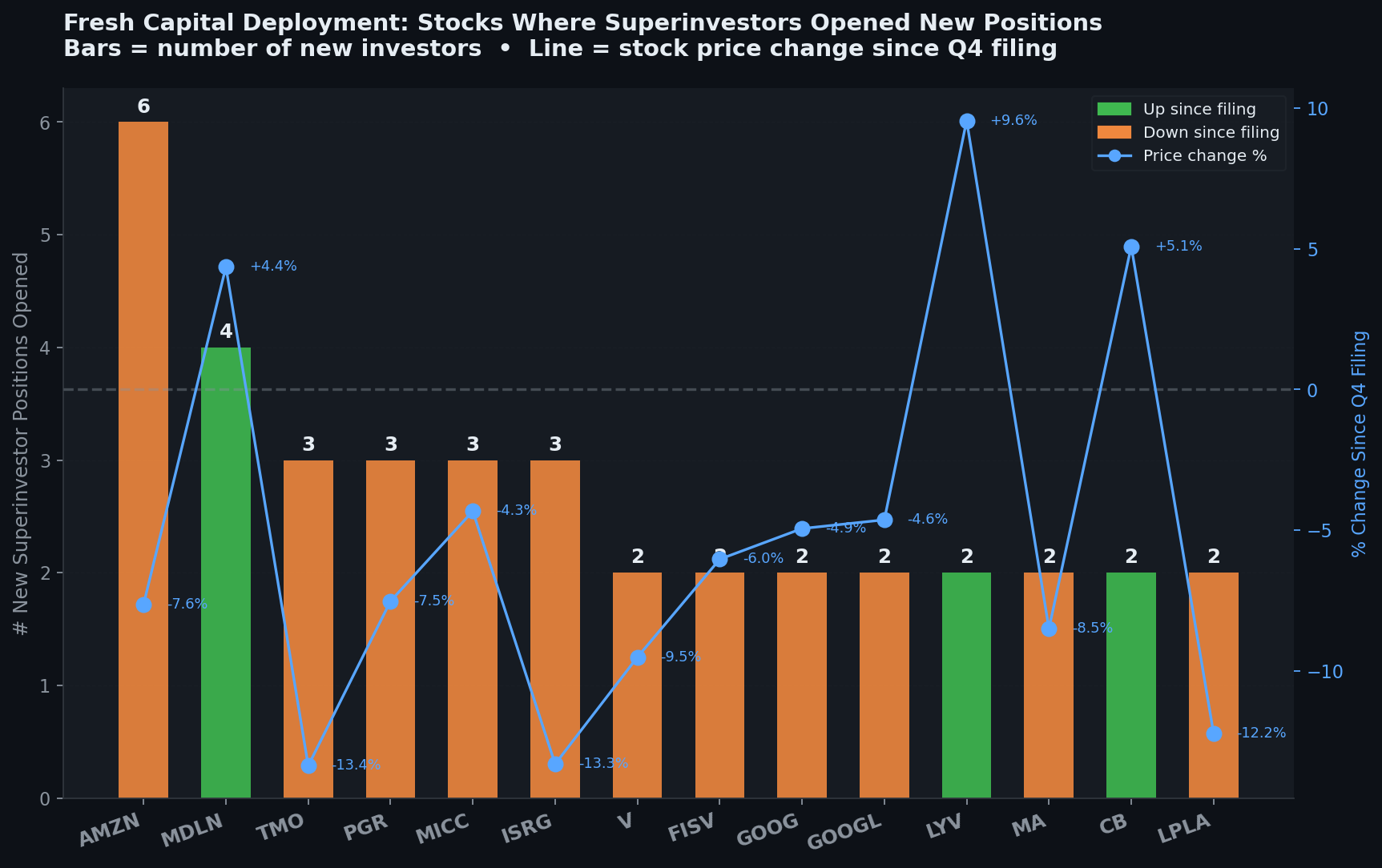

Chart 3: Fresh Capital Deployment — New Positions Only

Bars = number of new investors who opened a fresh position. Line = stock’s performance since the Q4 filing. Stocks below the line are cheaper now than when they bought.

The Hidden Gems: Fresh Money Flowing Into Overlooked Names

Medline Inc. (MDLN) — 4 Simultaneous New Buys

This is the most interesting signal in the entire dataset.

Four elite managers all opened brand new positions in Medline (MDLN) in Q4 2025: Henry Ellenbogen (Durable Capital), Lee Ainslie (Maverick Capital), Stephen Mandel (Lone Pine Capital), and Viking Global Investors.

Think about what it means for four of the most sophisticated institutional investors in the world to independently arrive at the same new idea in the same quarter.

Medline is the largest privately-held medical supplies company in the U.S. — or was. It went public in 2024 at $42/share. These managers are essentially making a bet on the intersection of healthcare infrastructure demand, aging demographics, and a freshly public company that’s still being discovered. At $43.83 (+4.4% since filing), the stock hasn’t run. You’re still close to the IPO price.

Current price: $43.83 | 52-week range: $34.89 – $50.88 | Since Q4 filing: +4.4%

Thermo Fisher Scientific (TMO) — 3 New Buys, 20%+ Below High

Three managers opened fresh TMO positions in Q4: Daniel Loeb, Steven Romick, and Viking Global — joined by two more who added to existing positions.

Thermo Fisher is the picks-and-shovels play on life sciences — if biotech does research, they buy Thermo Fisher equipment, reagents, and services. The stock got crushed in 2024-2025 as COVID testing revenue faded and biotech funding dried up. At $502, it’s -22% from its 52-week high of $644.

Daniel Loeb and Steven Romick are value-oriented managers who rarely buy biotech infrastructure without a margin of safety. They see one here.

Current price: $501.97 | 52-week range: $385 – $644 | Where it sits: 45% | Since Q4 filing: -13.4%

Progressive Corp (PGR) — 3 New Buys, AI-Driven Underwriting

Progressive is quietly one of the best-run insurance companies in America, famous for using data analytics for underwriting long before anyone called it “AI.” Three managers opened new positions in Q4: Bruce Berkowitz, Daniel Loeb, and Viking Global.

Insurance isn’t exciting — until you see 20%+ returns on equity sustained for a decade. Progressive’s telematics and risk selection are industry-leading, and the auto insurance pricing cycle is favorable after years of rate increases. At $249, it’s -9% from its high.

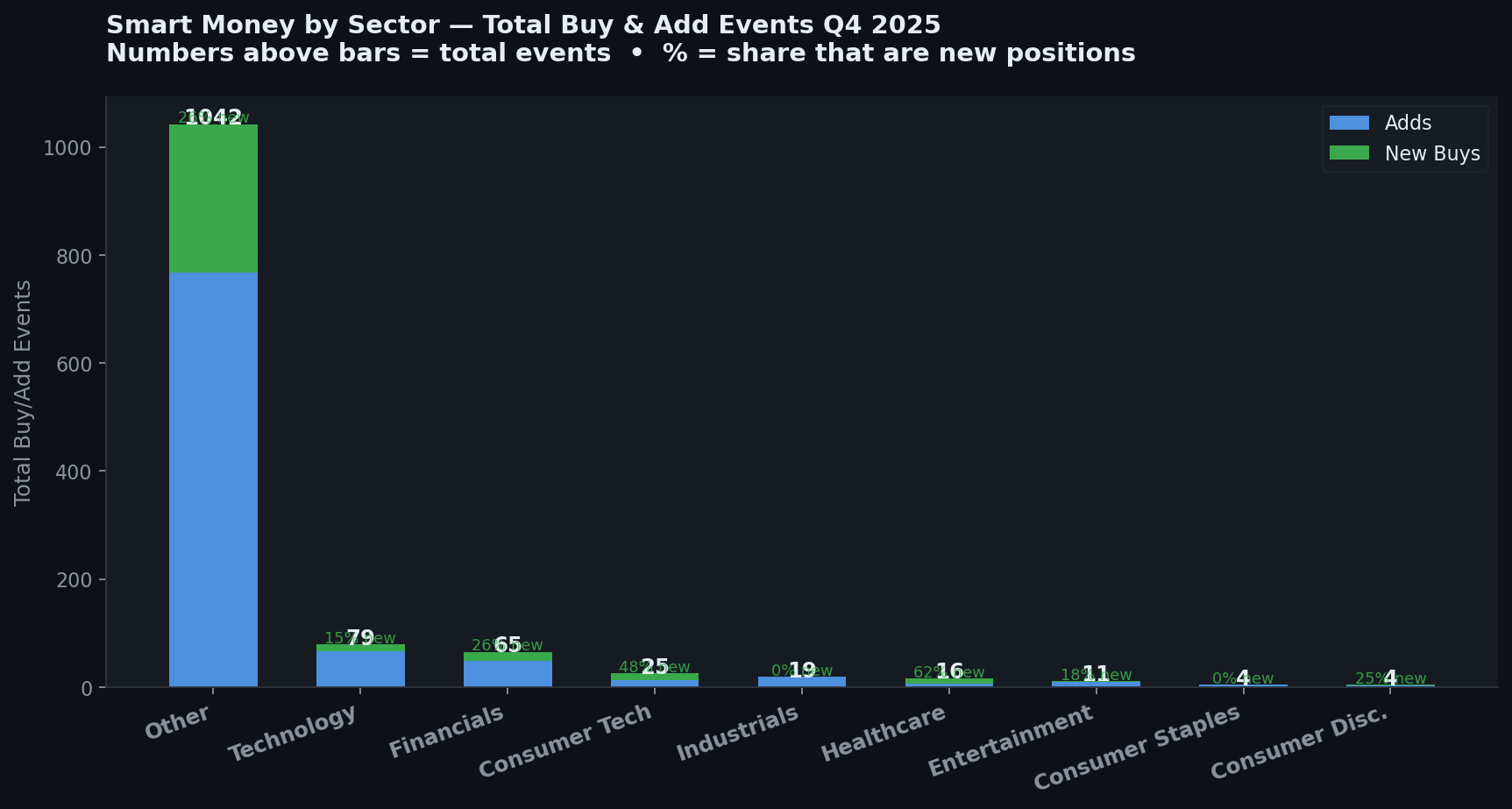

Chart 4: Where Is Smart Money Flowing by Sector?

Technology dominates — but notice how much of the activity is in financial infrastructure (Visa, Mastercard, SPGI, ICE, AON, Fiserv), healthcare picks-and-shovels (Thermo Fisher, ISRG, GEHC), and select industrials (Ferguson, Copart, Union Pacific). This isn’t pure growth chasing — it’s value-hunting across multiple sectors.

The Stocks Already Pricing In the Good News (Proceed With Caution)

Not every smart money buy is a current opportunity. These stocks have already moved substantially since the Q4 filings:

These are great businesses and the conviction behind them is real — but if you’re buying after a 10-12% run from already elevated prices, you’re paying more than the managers who tipped you off. TSM especially — at 80% of its 52-week range and +11.5% since filing — has meaningfully appreciated. The AI chip thesis is compelling, but the entry is less attractive today.

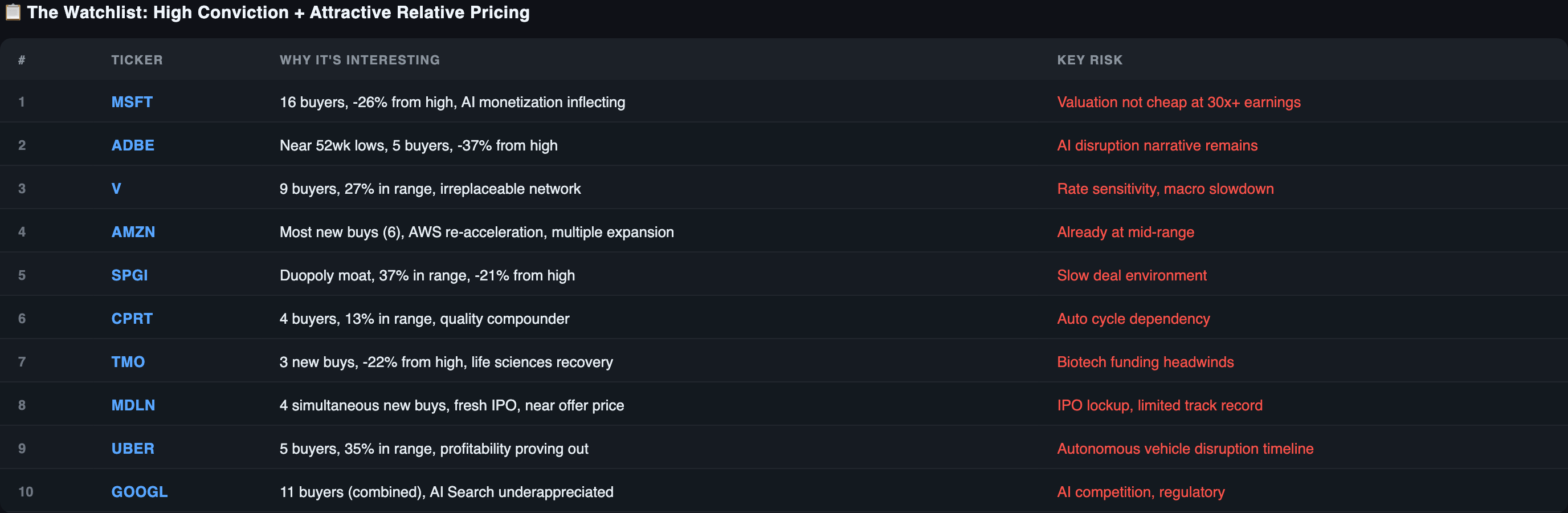

The Watchlist: My Takeaways

If I’m building a watchlist from this data, these are the names where high institutional conviction meets attractive relative pricing:

One Final Thought

13-F analysis is a lagging indicator — by definition, you’re looking at what managers held 45-90 days ago. Positions can change. But the signal isn’t about timing — it’s about identifying where institutional intelligence has clustered.

When 16 of the world’s best investors add to the same stock in the same quarter, and that stock has since gotten cheaper, that convergence is worth taking seriously.

The market has given you lower prices than the smartest money in the world paid. What you do with that is up to you.

Data sourced from Dataroma.com Q4 2025 13-F filings. All prices as of early March 2026. This is not financial advice. Past superinvestor activity does not guarantee future returns. Always do your own research before making investment decisions.

If this was useful, consider sharing it. The next edition will dig deeper into the individual position sizes and portfolio concentration — where managers are putting their largest bets.