GitLab Hit $1B ARR. Then the Guidance Hit Wall Street.

Q4 FY2026 breakdown: Revenue beat, record $1M+ customers, and a FY2027 EPS guide that missed by 25%.

GitLab just achieved what no pure-play DevSecOps platform had done before — $1 billion in annual recurring revenue. They beat on revenue, crushed EPS estimates, and announced a $400 million share buyback. The stock fell 5% anyway. Here’s why.

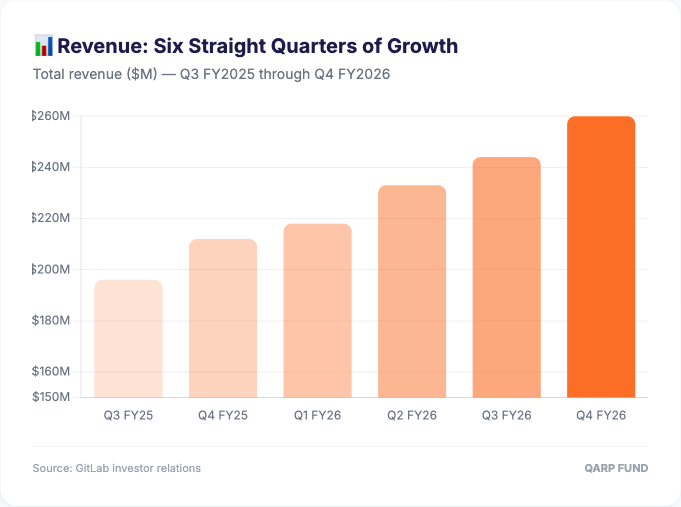

📊 Revenue: Six Straight Quarters of Growth

GitLab closed Q4 FY2026 with $260.4M in revenue (+23% YoY), beating the $252.2M estimate by $8.2M. Full-year FY2026 revenue hit $955.2M (+26% YoY) — just shy of the $1 billion annual mark.

GitLab delivered a clean Q4 beat. Revenue, EPS, and gross margins all came in above estimates. The problem: FY2027 guidance.

Revenue beat: $260.4M vs. $252.2M est ✅

Non-GAAP EPS beat: $0.30 vs. $0.23 est ✅

FY27 EPS guide: $0.76–$0.80 vs. $1.05 consensus ❌ (25%+ miss)

FY27 Revenue guide: $1.10–$1.12B vs. $1.12B est (slight miss)

Management is making a deliberate choice: invest heavily in the Duo Agent Platform, compress near-term margins, and bet on the AI developer tools wave. Reasonable strategy. Markets wanted more profitability now.

🔮 FY2027 Outlook: Revenue On Track, Margins Under Pressure

Q1 FY2027 Revenue: $253–$255M (seasonal step-down)

Full Year FY2027 Revenue: $1.10–$1.12B (~16% growth)

Full Year FY2027 EPS: $0.76–$0.80 (vs. $1.05 est — big miss)

$400M buyback: First ever — signals long-term confidence

CEO Bill Staples: “GitLab sits at the heart of how enterprises build and deliver software.” The Duo Agent Platform aims to automate developer workflows — a direct play on the AI coding wave that’s reshaping enterprise software.

⚡ The Bottom Line

GitLab had a genuinely strong Q4. The $1B ARR milestone is meaningful. The $400M buyback shows management confidence. Enterprise customer growth at the $1M+ tier is accelerating.

But the 25% EPS guidance miss is hard to ignore. Markets are pricing in profitable growth, and GitLab is choosing investment over profitability for FY2027. The question: does the Duo Agent Platform accelerate the growth story — or is this a margin drag that delays the payoff?

Watch the net retention rate. 118% is solid. If Duo drives it above 120% in FY2027, the AI investment is working. If it slips, the mid-market and SMB pressure is the real story.

Follow @qarpfund for weekly earnings analysis

Until next time,

Qarp FundQ4 Revenue: $260.4M vs. $252.2M est (+$8.2M beat)

Full Year FY2026: $955.2M (+26% YoY)

Gross Margin: 89% non-GAAP — world-class software economics

RPO: $1.1B total (+20% YoY), O $719.4M (+24% YoY)

Six consecutive quarters of sequential growth. The RPO acceleration signals future revenue is being locked in ahead of schedule.

🎯 Enterprise Customers: The $1M+ Cohort Is Accelerating

GitLab added the largest number of million-dollar ARR customers in company history in Q4. Enterprise platform consolidation is working.

$5K+ ARR customers: 10,682 (+8% YoY)

$100K+ ARR customers: 1,456 (+18% YoY)

$1M+ ARR customers: 155+ — record additions

The acceleration at the top of the funnel is exactly what a platform consolidation story looks like. Enterprises are replacing multiple dev tools with GitLab as their single DevSecOps platform.