Copart Inc. (CPRT): The Auto Auction King Riding the Wave of Vehicle Complexity

Executive Summary

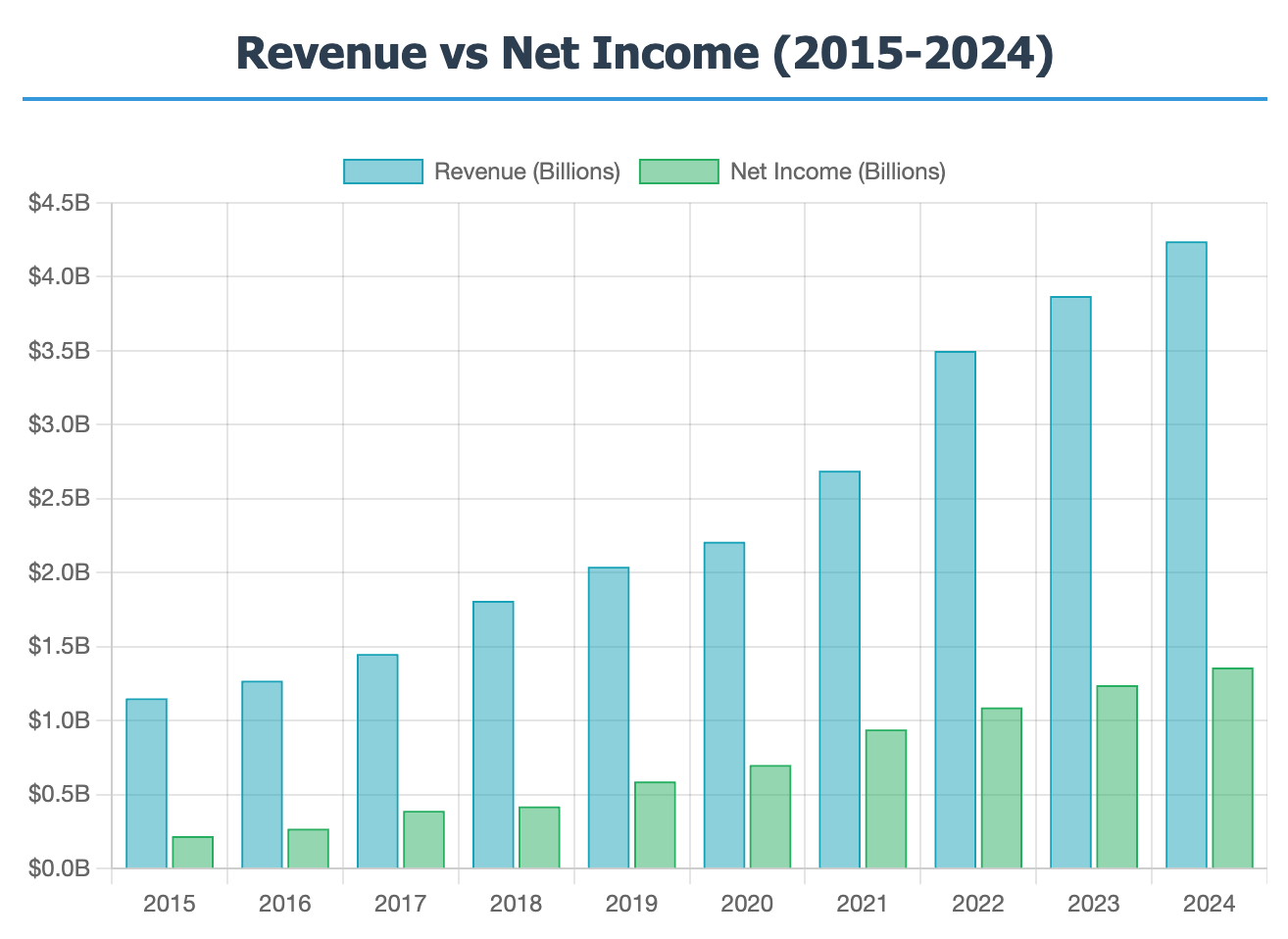

Copart Inc. (NASDAQ: CPRT) stands as the undisputed leader in the online vehicle auction industry, commanding approximately 40% market share in the American automotive auction market. In 2025, Copart maintains a commanding position in the American automotive auction market. The company accounts for nearly 40% of the industry's market share. With fiscal 2024 revenue reaching $4.24 billion and net income of $1.36 billion, the company has demonstrated remarkable consistency in both growth and profitability over the past two decades.

Key Investment Highlights:

Market-leading position with significant competitive moats

Exceptional financial performance with 32% net margins

Strong secular tailwinds from increasing vehicle complexity

Robust free cash flow generation ($965M in fiscal 2024)

Trading at 34x P/E ratio reflecting premium valuation

Company Overview

Founded in 1982, Copart operates the world's largest online vehicle auction platform, processing over 4 million vehicles annually across 11 countries through more than 250 locations. The company primarily serves insurance companies by auctioning vehicles declared total losses, but has expanded to serve banks, rental companies, fleet operators, and individual consumers.

Business Model Strengths

Copart's asset-light model acts as a marketplace rather than taking inventory risk. The company generates revenue through:

Service fees from vehicle processing and storage

Auction fees charged to buyers and sellers

Transportation and logistics services

Additional services like parts sales and vehicle inspections

Financial Performance Analysis

Revenue Growth Trajectory

Copart has delivered exceptional long-term growth, with revenue expanding from $254 million in fiscal 2001 to $4.24 billion in fiscal 2024 - a compound annual growth rate of approximately 13%. The growth has been particularly impressive over the past five years:

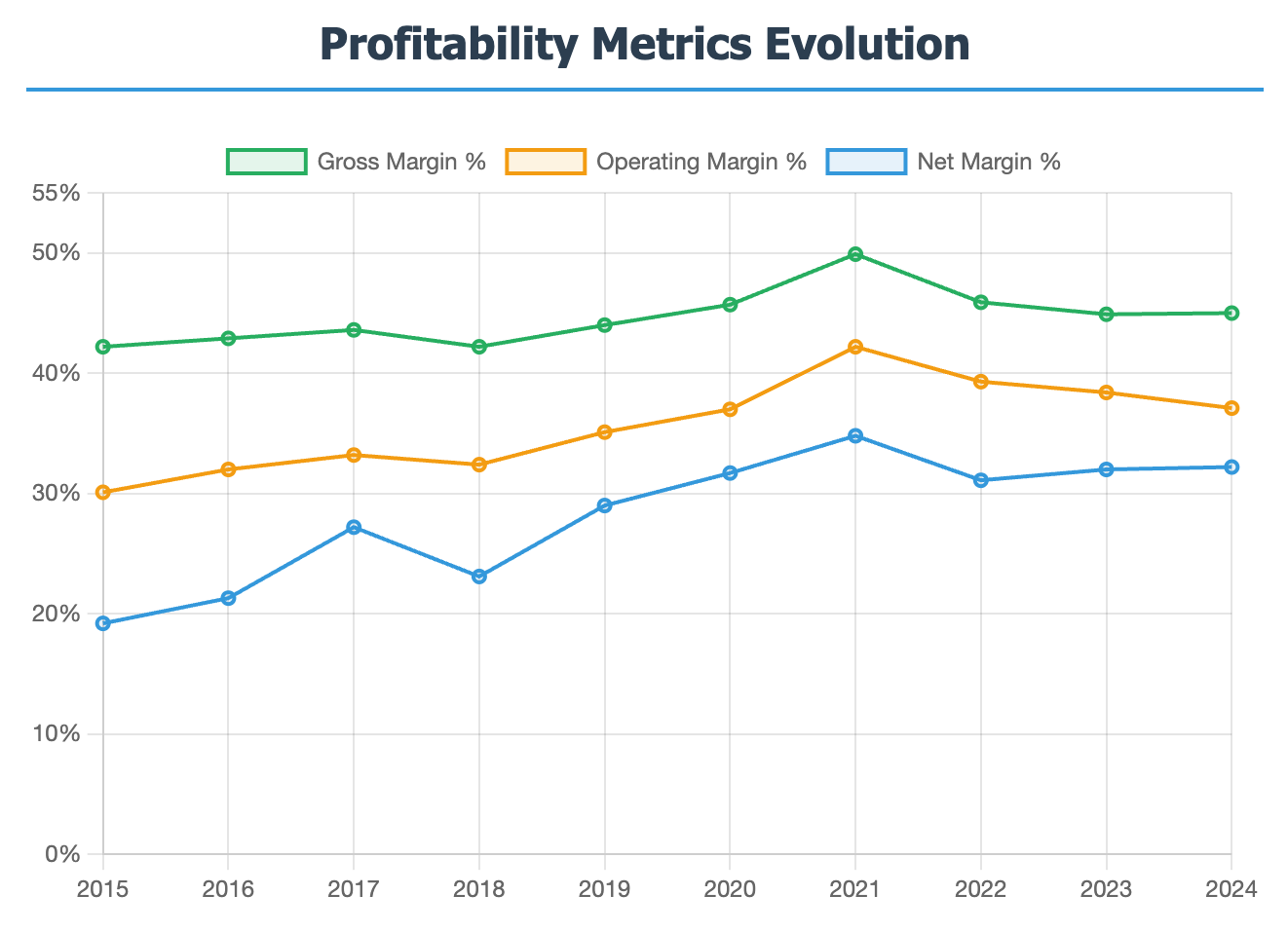

Profitability Excellence

One of Copart's most impressive characteristics is its consistent profitability improvement. Net margins have expanded from 16.8% in fiscal 2001 to 32.2% in fiscal 2024, demonstrating exceptional operational leverage:

Key Profitability Metrics (Fiscal 2024):

Gross Margin: 45.0%

Operating Margin: 37.1%

Net Margin: 32.2%

Return on Equity: 20.2%

Return on Assets: 18.0%

Balance Sheet Strength

Copart maintains a fortress-like balance sheet with minimal debt and substantial cash reserves:

Balance Sheet Highlights (Fiscal 2024):

Total Assets: $8.43 billion

Cash and Equivalents: $1.51 billion

Total Debt: $0 (essentially debt-free)

Shareholders' Equity: $7.52 billion

Current Ratio: 8.2x

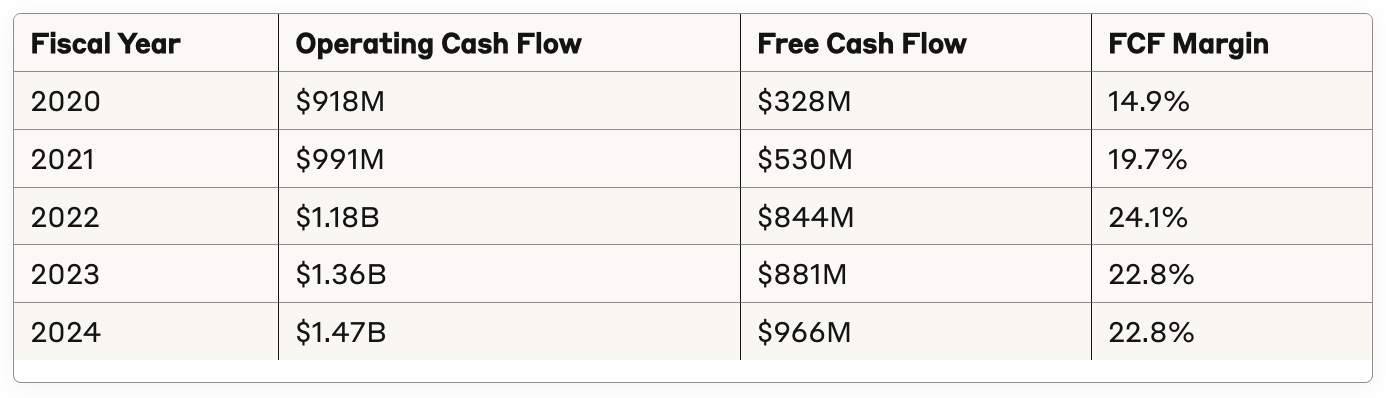

Cash Generation Machine

The company consistently generates substantial free cash flow, converting earnings into cash efficiently:

Industry Dynamics and Competitive Position

Market Structure

The North American salvage vehicle auction market is highly consolidated, with the top two competitors, Copart and IAAI, representing an estimated 37% and 35% of the market, respectively, and no other competitor representing more than 10%. This duopoly structure provides significant competitive advantages.

Secular Growth Drivers

Several powerful trends support Copart's long-term growth prospects:

Vehicle Complexity Increases Total Loss Rates The expense of fixing vehicles, which are replete with computer chips, ADAS equipment and advanced electronics, is less enticing to insurance companies than paying out the vehicle's worth. Modern vehicles contain increasingly sophisticated technology that makes repairs more expensive than replacement.

Record Total Loss Frequency The full-year trend of 22.2% represents an all-time annual high, and the total loss frequency drivers certainly continue unabated. This trend is expected to continue as vehicles become more complex.

Natural Disasters and Climate Events Catastrophic events from late last year, including hurricanes Milton and Helene, contributed to the increased number of totaled vehicles. Climate change is increasing the frequency and severity of weather-related vehicle damage.

Competitive Advantages

Copart benefits from several defensive moats:

Network Effects: More buyers attract more sellers, and vice versa

Scale Economies: Fixed costs spread across millions of vehicles

Land Ownership: Strategic real estate positions near population centers

Technology Leadership: Proprietary VB3 auction platform and Copart 360 imaging

Switching Costs: Integrated relationships with insurance companies

Recent Performance and Management Commentary

Q2 2025 Results Highlights

Copart beat Wall Street's expectations in Q1 2025 and has exceeded expectations for three of the past five quarters. Recent quarterly performance showed:

Global volume growth: 8% year-over-year in Q2 2025

Blue Car service growth: Exceeded 27% year-over-year

Purple Wave growth: 8% growth in heavy machinery and farming equipment auctions

However, the stock faced some pressure after recent earnings: Shares of leading online vehicle auction platform Copart (CPRT -1.40%) were down 12% as of noon ET Friday, according to data provided by S&P Global Market Intelligence. Copart reported earnings on Friday and delivered sales and earnings per share growth of 8%. This top-line figure missed analysts' expectations, and the stock sold off as a result.

International Operations

Copart's international expansion continues, though with mixed results. Abroad, the company reported that international purchased vehicle revenue decreased by over $18 million or 22%. However, this was accompanied by an increase in gross profit, partly due to changes in the business model in Germany and stronger margins in the UK.

Risk Factors and Challenges

Near-term Headwinds

Uninsured Population Growth The company acknowledged a "modest increase in the uninsured population relative to pre-COVID levels." Fewer insured vehicles could disrupt the company's flow of totaled cars and parts into its marketplaces.

Tariff Uncertainty While management believes tariffs could be neutral to positive for business, President Donald Trump announced potential tariffs on all Canadian and Mexican imports, starting March 4. The added taxes could impact Copart's underlying numbers, potentially increasing repair costs while also raising pre-accident values.

Valuation Concerns Trading at 43 times earnings prior to the report, Copart was priced with the lofty expectation that it'd continue growing sales by its historical double-digit average, and came up just shy.

Long-term Considerations

Electric vehicle adoption could change salvage patterns

Autonomous vehicle technology may reduce accident rates

Economic downturns could impact vehicle sales and insurance coverage

Valuation Analysis

Current Metrics

Trading Statistics (as of June 2025):

Stock Price: $50.13

Market Cap: $49.7 billion

Trailing P/E: 34.1x

Forward P/E: 29.6x

Price-to-Sales: 10.8x

Price-to-Book: 5.7x

Enterprise Value/EBITDA: ~25x

Historical Context

Copart has historically traded at premium valuations due to its:

Dominant market position

Consistent growth track record

High-quality business model

Strong competitive moats

Since going public in 1994, Copart has become a 398-bagger, generating an annualized total return of 21%.

Forward-Looking Considerations

The current valuation appears demanding but may be justified by:

Continued secular growth in total loss rates

International expansion opportunities

Adjacent market penetration (Purple Wave, Blue Car)

Technology-driven efficiency gains

Investment Recommendation

Rating: HOLD with a bias toward BUY on weakness

Copart represents one of the highest-quality businesses in the public markets, with an exceptional track record of growth and profitability. The company benefits from powerful secular tailwinds that should drive growth for years to come.

Bull Case

Market-leading position with significant moats

Secular growth from increasing vehicle complexity

Strong balance sheet enables opportunistic expansion

Technology leadership drives operational efficiency

International expansion provides long-term upside

Bear Case

Premium valuation leaves little room for disappointment

Cyclical headwinds from insurance industry dynamics

Potential disruption from autonomous vehicles

Economic sensitivity despite defensive characteristics

Target Price and Recommendation

Based on historical valuations and growth prospects, a fair value range of $52-58 per share appears reasonable, representing 25-30x forward earnings on estimated 2026 EPS of $2.00-2.20.

Action: Current investors should hold their positions, while new investors should consider building positions on any weakness below $48 per share. The combination of secular growth trends and market leadership makes Copart an attractive long-term holding despite current valuation concerns.

Conclusion

Copart Inc. stands as a testament to the power of network effects and market leadership in creating sustainable competitive advantages. While the current valuation reflects high expectations, the company's position at the intersection of several powerful secular trends - vehicle complexity, climate change, and digitalization - provides a compelling long-term investment thesis.

The recent stock weakness following earnings presents an opportunity for patient investors to add to positions in one of the market's highest-quality compounding machines. With its debt-free balance sheet, consistent cash generation, and dominant market position, Copart is well-positioned to continue delivering superior returns to shareholders over the long term.

Disclaimer: This analysis is for informational purposes only and should not be considered as investment advice. Please conduct your own research and consult with a financial advisor before making investment decisions.