AutoZone Beats EPS — But the Market Hit the Brakes Anyway

Sales up 8%, EPS beats by $0.22 — but a $79M revenue miss and margin compression sent AZO down 6.7%

AutoZone just reported Q2 FY2026 earnings, and the headline numbers tell two different stories. Revenue grew 8% year-over-year. EPS technically beat estimates. And yet the stock fell nearly 7% on the day. So what happened?

📊 Sales Growth Remains Solid

AutoZone posted $4.27 billion in net sales for Q2 FY2026 (the 12-week period ending February 14, 2026), an increase of 8.1% year-over-year. That's the kind of steady growth you'd expect from a company selling parts for the nearly 300 million cars on American roads.

But Wall Street was looking for $4.35 billion — and the $79 million gap is what drove the selloff.

Net Sales: $4.27B (+8.1% YoY)

Net Income: $468.9M (down from $487.9M a year ago)

YTD Revenue: $8.9B through the first 24 weeks of fiscal 2026

Worth noting: Q4 FY2025's enormous $6.24B reflects AutoZone's longer 16-week fiscal fourth quarter — not a sudden surge in business.

🎯 EPS Beat, Revenue Miss — Market Chose the Miss

Here's the split verdict from Q2:

EPS: $27.63 vs. $27.41 estimate → Beat by $0.22

Revenue: $4.27B vs. $4.35B estimate → Missed by $79M

The EPS beat matters less when gross margins are shrinking. Net income fell to $468.9M from $487.9M — a $19M drop year-over-year despite 8% revenue growth. The market read that as a signal that AutoZone's profitability engine is under stress.

Stock closed down 6.7% on March 3, 2026.

🏪 The Cars Are Coming In. Comps Are Growing.

The underlying demand story is healthy. Comparable store sales (SSS) grew across all geographies:

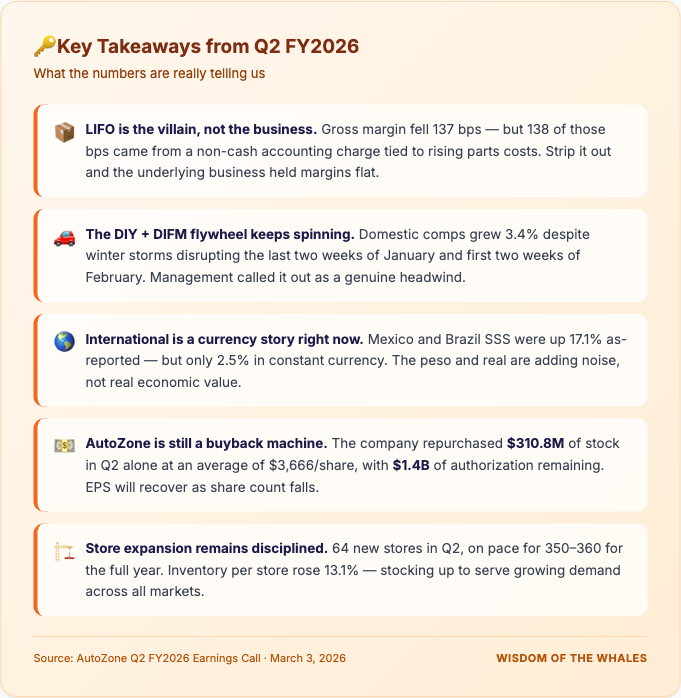

Domestic: +3.4% (despite winter storms in late January and early February)

International (constant currency): +2.5%

Total Company (constant currency): +3.3%

Management flagged winter storms as a meaningful headwind in the back half of Q2. Auto parts demand is highly weather-correlated — storms suppress DIY repair activity. The fact that comps stayed positive through those disruptions speaks to the durability of AutoZone's customer base.

The international headline number looks eye-popping at +17.1% — but that's a currency translation effect, not operational outperformance. In constant currency, it was a solid but unspectacular +2.5%.

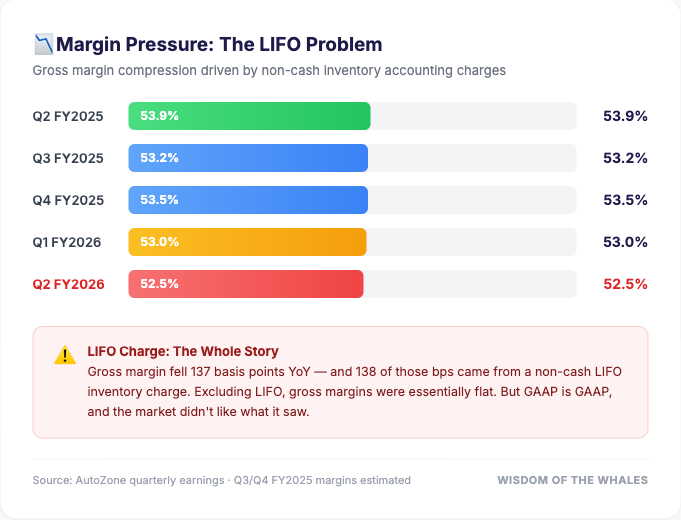

📉 Margin Compression: Blame the Accounting, Not the Business

This is the number that spooked investors: gross margin fell to 52.5%, down 137 basis points year-over-year.

But here's the key detail: 138 of those 137 basis points came from a single non-cash LIFO charge.

LIFO (Last In, First Out) inventory accounting means that when parts costs rise, AutoZone's cost of goods sold reflects the higher-priced inventory first — even if those parts haven't actually been sold yet. It's an accounting methodology, not a cash expense. Excluding LIFO, gross margins were essentially flat year-over-year.

The business is fine. The accounting treatment is making it look worse than it is. But GAAP is GAAP, and analysts aren't ignoring the trend.

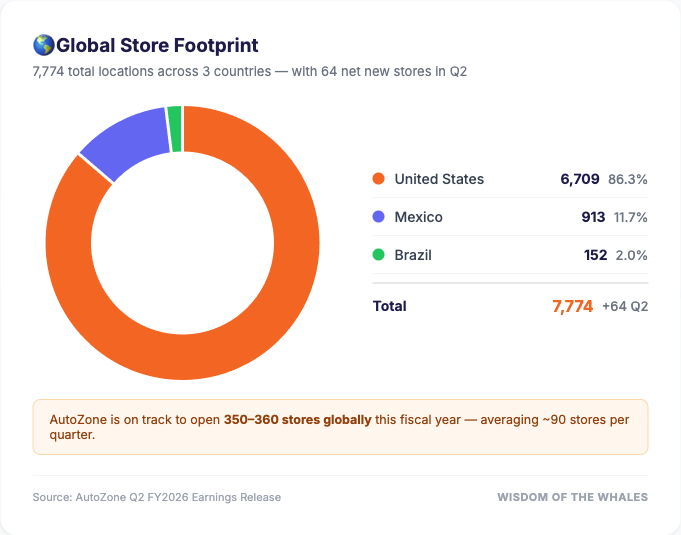

🌎 7,774 Stores and Still Expanding

AutoZone opened 64 net new stores in Q2, staying firmly on track for its full-year target of 350–360 new locations globally.

The US footprint dominates at 6,709 stores (86% of total), but Mexico (913 stores) and Brazil (152 stores) represent the growth runway. International expansion is the long game — and AutoZone is playing it methodically.

One flag worth watching: inventory per store grew 13.1% year-over-year. That reflects deliberate stocking decisions in anticipation of demand — but it also means capital tied up in shelves, contributing to the LIFO charge problem.

🔑 The Numbers Behind the Numbers

⚡ The Bottom Line

AutoZone's Q2 FY2026 was a tale of optical vs. operational performance. The business grew 8%. Comps stayed positive through weather disruptions. New stores opened on schedule. And a $310.8M share buyback program is steadily reducing the share count.

But a non-cash accounting charge made margins look terrible, a $79M revenue shortfall disappointed analysts, and the stock got punished accordingly.

The bears will point to the margin trend and wonder if the LIFO charges keep coming. The bulls will note that ex-LIFO, the business is performing as expected — and that a shrinking float and disciplined expansion point toward EPS recovery.

With $1.4 billion of buyback authorization remaining and a store count approaching 8,000, AutoZone's flywheel is intact. Whether the stock recovers depends on whether the LIFO headwind becomes the story — or just a footnote.

Until next time,

Qarp Fund