ASML Deep Dive: The Monopoly Powering the AI Revolution

ASML continues to dominate the semiconductor equipment industry with its monopoly on EUV lithography technology.

Executive Summary

ASML continues to dominate the semiconductor equipment industry with its monopoly on EUV lithography technology. Despite Q1 2025 bookings coming in below expectations at $4.4 billion, the company maintains strong fundamentals with 54% gross margins and guides for $34-40 billion in 2025 revenue. Trading at a P/E of 29.7x, ASML commands a premium valuation justified by its technological moat and exposure to AI-driven semiconductor demand.

The Numbers That Matter

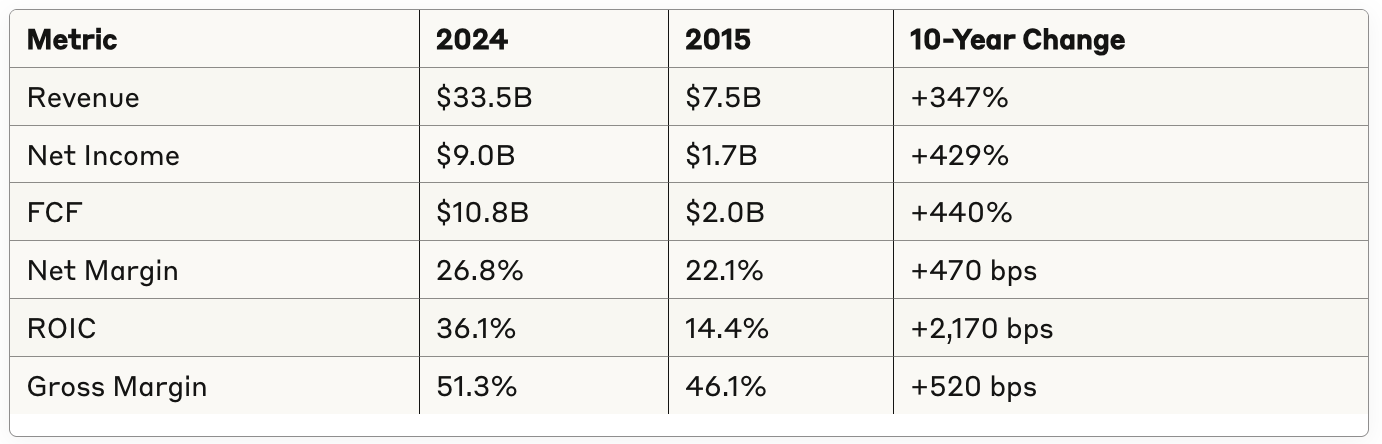

Financial Performance (2024 vs 2015)

Q1 2025 Update

ASML reported Q1 2025 results on April 16, 2025:

Revenue: $8.7 billion (in line with guidance)

Gross Margin: 54.0% (above 50-52% guidance)

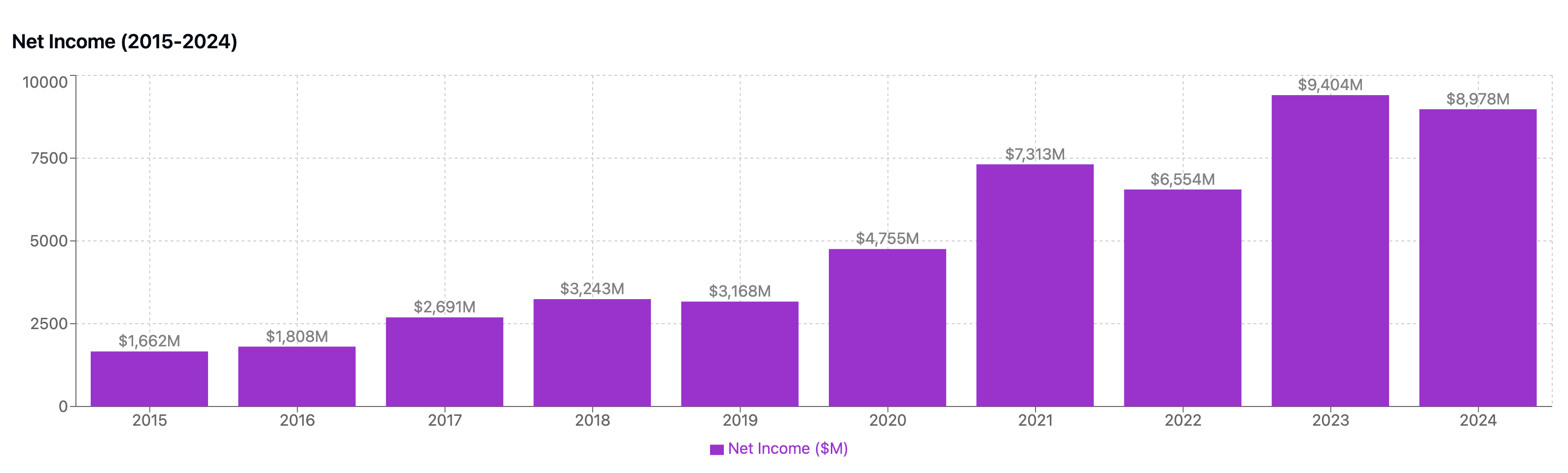

Net Income: $2.7 billion

Net Bookings: $4.4 billion (below $5.5B consensus)

EUV Bookings: $1.4 billion of total bookings

The Monopoly Moat

ASML's competitive advantage is unparalleled in the semiconductor industry:

100% market share in EUV lithography - No viable competitors

80%+ market share in ArF immersion - Critical for advanced nodes

Installed base of 500+ systems generating recurring revenue

15+ years ahead of competition in EUV technology

Technology Leadership by the Numbers

Financial Strength

Key Metrics Excellence

Interest Coverage

With $15.1B in cash and minimal debt, ASML has fortress-like balance sheet strength. Interest coverage exceeds 100x, providing complete financial flexibility.

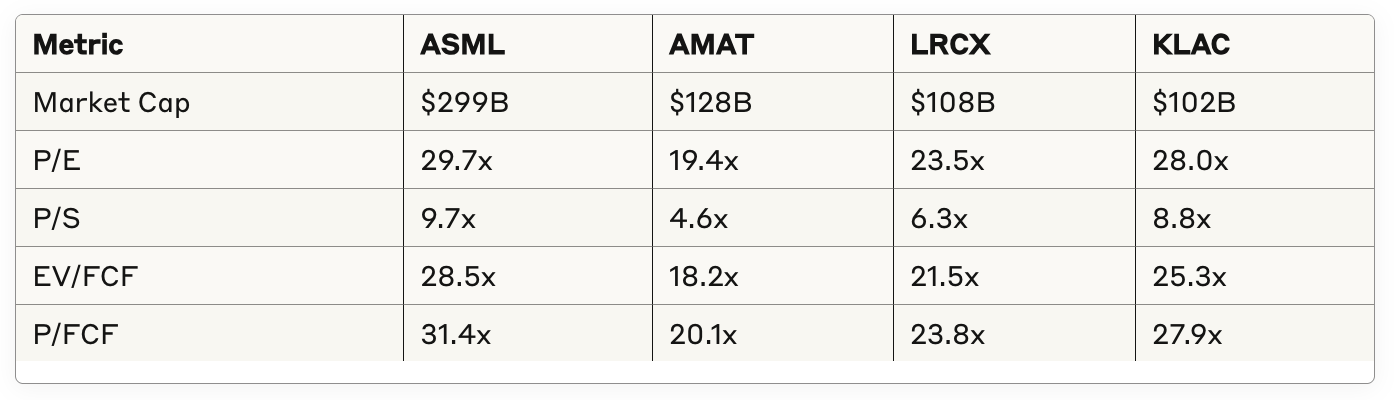

Valuation Analysis

Current Valuation Metrics

Valuation Premium Justified By:

Monopoly position in critical technology

Superior margins (51%+ gross margins vs 40-45% for peers)

Higher growth potential from AI and advanced nodes

Pricing power with 3-5 year order backlogs

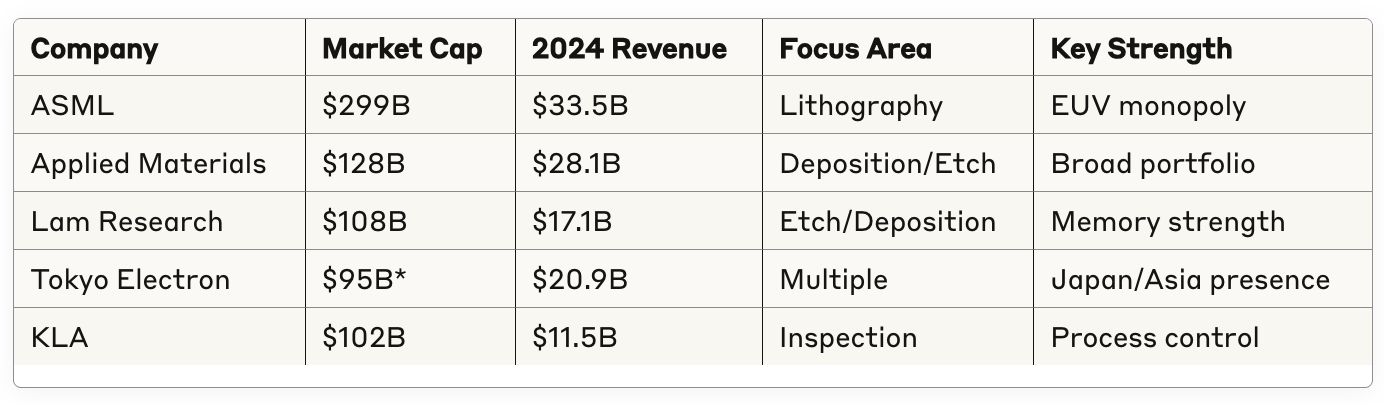

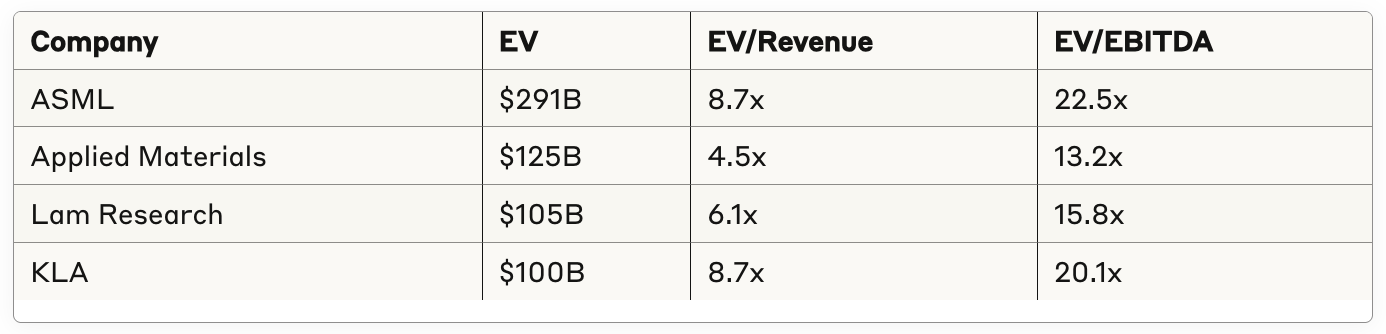

Competitive Landscape

Market Position vs Key Competitors

*Estimated based on market data

Enterprise Value Comparison

Growth Catalysts

1. AI Semiconductor Boom

AI chips require most advanced nodes (3nm, 2nm)

Each new node requires 2-3x more EUV layers

High-NA EUV adoption starting in 2025-2026

2. Geographic Expansion

$34-40B 2025 guidance implies 1-19% growth

China represented 32% of Applied Materials revenue

ASML less exposed but benefits from global capacity adds

3. Technology Transitions

GAA (Gate-All-Around) requiring more lithography steps

Advanced packaging needing lithography equipment

Emerging memories (HBM, MRAM) driving tool demand

Risk Factors

1. Geopolitical Tensions

Export restrictions to China (though ASML has exemptions)

Tariff uncertainties impacting customer spending

Regional semiconductor capacity buildouts

2. Cyclical Exposure

Memory spending remains volatile

Customer concentration (TSMC, Samsung, Intel)

Long lead times amplify cycle impacts

3. Valuation Risk

Trading at 10-year high multiples

Limited upside if growth disappoints

Competition in DUV from Canon/Nikon

Investment Thesis

Bull Case (Target: $1,075)

AI drives sustained 15%+ revenue CAGR

High-NA EUV adoption exceeds expectations

Gross margins expand to 55%+ by 2026

Multiple expansion to 35x P/E on monopoly premium

Base Case (Target: $935)

10-12% revenue CAGR through 2027

Steady margin improvement to 52-53%

Current multiples maintained

Continued technology leadership

Bear Case (Target: $735)

Cyclical downturn deeper than expected

China restrictions expanded

Gross margins compress to 48-50%

Multiple compression to 25x P/E

The Bottom Line

ASML remains the crown jewel of semiconductor equipment with an unassailable competitive position. While near-term bookings disappointed and tariff uncertainties loom, the company's monopoly on EUV technology makes it indispensable for advancing Moore's Law.

For long-term investors: ASML offers exposure to secular semiconductor growth with pricing power few companies possess. The premium valuation is justified by superior returns and competitive positioning.

For traders: Wait for pullbacks below $720 for better entry points given elevated valuations and near-term uncertainties.

Overall Rating: BUY with a 12-month target of $935 (21% upside)

Key Takeaways:

Monopoly business model with 50%+ gross margins

ROIC of 36% demonstrates exceptional capital efficiency

$10.8B in 2024 FCF provides ample capital return flexibility

AI semiconductor demand provides multi-year growth runway

Premium valuation justified but limits near-term upside

Disclosure: This analysis is for informational purposes only and not investment advice. Do your own research before making investment decisions.